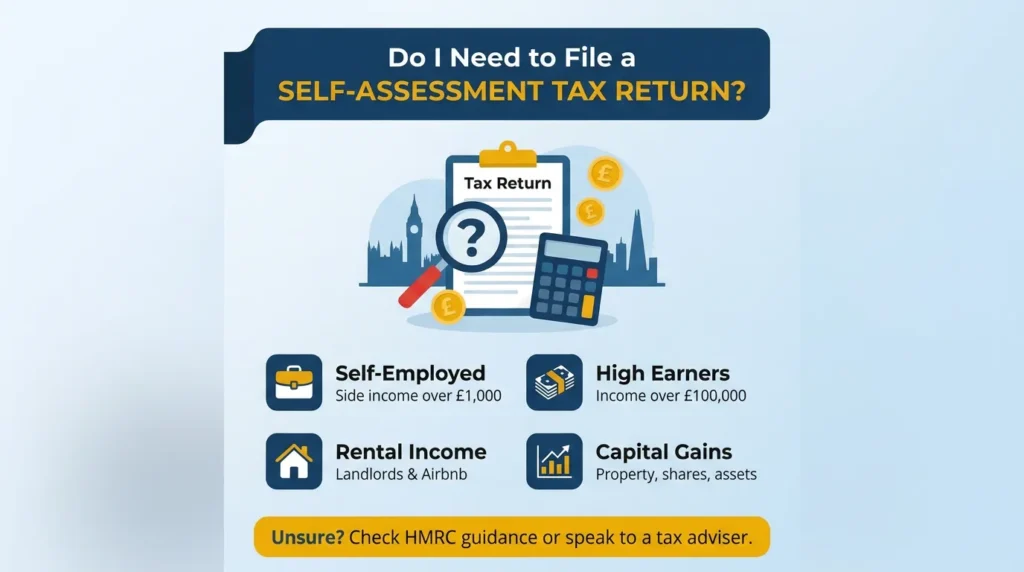

If you’re asking, “Do I need to file a Self Assessment Tax Return?”, you’re not alone.

UK tax rules can feel confusing, especially if you have a side income, rental property, or earnings over £100,000.

The simple rule is this:

You must file a Self Assessment Tax Return if you have income that HMRC cannot automatically collect through PAYE.

This guide explains who needs to file, when to register, and what risks to avoid, clearly and without jargon.

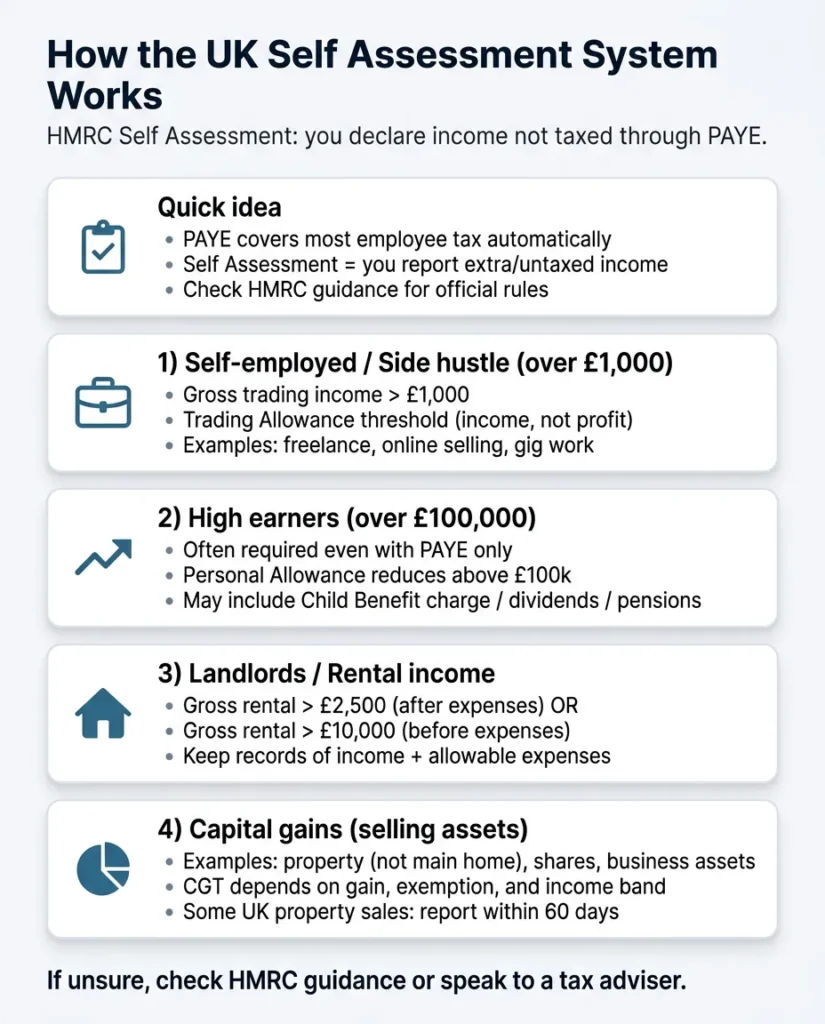

How the Self Assessment System Works

The UK operates a Self Assessment system managed by HM Revenue and Customs (HMRC).

Most employees pay tax automatically through PAYE (Pay As You Earn). But if you earn income that is not taxed at source, you are responsible for declaring it.

Official HMRC guidance can be found here

Let’s look at the most common situations where filing is required.

1. Self-Employed or Side Hustle Income (Over £1,000)

If you are self-employed and your gross trading income exceeds £1,000 in a tax year, you must register for Self Assessment.

This applies to:

- Freelancers

- Consultants

- Contractors

- Online sellers (eBay, Etsy, Amazon)

- Gig economy workers

- Anyone earning from a side hustle

The £1,000 threshold refers to total income, not profit. This is called the Trading Allowance.

If your income is below £1,000, you may not need to file, but accurate record-keeping is still essential.

2. High Earners (Income Over £100,000)

If your adjusted net income exceeds £100,000, you will usually need to submit a Self Assessment Tax Return, even if all your income is taxed through PAYE.

Why?

Because:

- Your Personal Allowance is reduced above £100,000

- Additional tax adjustments may apply

- HMRC requires full income disclosure

High earners may also need to report:

- Child Benefit High Income Charge

- Pension contribution limits

- Dividend income

- Additional rate tax exposure

At this income level, filing ensures your tax position is accurate and compliant.

3. Landlords and Rental Income

If you receive rental income, you may need to file if:

- Your gross rental income exceeds £2,500 after expenses, or

- Your gross rental income exceeds £10,000 before expenses

This applies to:

- Buy-to-let landlords

- Accidental landlords

- Overseas property owners

- Airbnb hosts

Allowable expenses may include mortgage interest (subject to Section 24 rules), agent fees, maintenance, and repairs.

Accurate reporting protects both compliance and tax efficiency.

4. Capital Gains (Selling Assets)

You may need to report Capital Gains if you sell:

- Property (other than your main residence)

- Shares or investments

- Business assets

Capital Gains Tax depends on:

- The type of asset

- The size of the gain

- Your available annual exemption

- Your overall income level

Some UK property sales must be reported within 60 days, even before the annual Self Assessment deadline.

If you are unsure whether a disposal creates a reporting obligation, professional advice is sensible.

Registering vs Filing – What’s the Difference?

Many people confuse these steps.

Registering for Self Assessment

- This is a one-time notification to HMRC that you need to file.

- You receive a Unique Taxpayer Reference (UTR).

- You must register by 5 October following the end of the tax year in which you became liable.

Filing the Tax Return

- This is the annual submission of your income details.

Deadlines:

- 31 October (paper return)

- 31 January (online return and payment deadline)

Missing these dates results in automatic penalties.

What Happens If You File Late?

HMRC applies structured penalties:

- £100 automatic fine for missing the deadline (even if no tax is owed)

- Daily penalties after 3 months

- Interest on unpaid tax

The system is strict, but avoidable. Filing early reduces risk.

Who Usually Does NOT Need to File?

You may not need to file if:

- You are employed under PAYE only

- You have no additional untaxed income

- HMRC has not issued a notice to file

However, if HMRC formally requests a return, you must respond, even if you believe no tax is due.

When Should You Seek Professional Advice?

Consider professional guidance if you:

- Have multiple income sources

- Cross the £100,000 threshold

- Recently became self-employed

- Have undeclared past income

- Sold a high-value asset

- Earn foreign or dividend income

A compliance review provides clarity and reduces the risk of penalties.

Key Takeaway

You likely need to file a Self Assessment Tax Return if you:

- Earn over £1,000 from self-employment

- Have an income over £100,000

- Receive rental income above reporting thresholds

- Made capital gains

- Have untaxed dividend or foreign income

If none of these applies and your tax is fully managed through PAYE, you may not need to file.

When in doubt, check official HMRC guidance or seek professional advice. Filing correctly is not about fear; it is about staying compliant and in control.

Unsure If You Meet the Criteria?

If you are still unsure whether you need to file, a brief compliance review can provide clarity.

For tailored guidance, contact Protax Consultants

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record