If you’re unsure what income must be declared on a Self Assessment tax return, you’re not alone. Many UK taxpayers, especially freelancers, landlords, directors and high earners, are unclear about what counts as taxable income.

The core rule is simple:

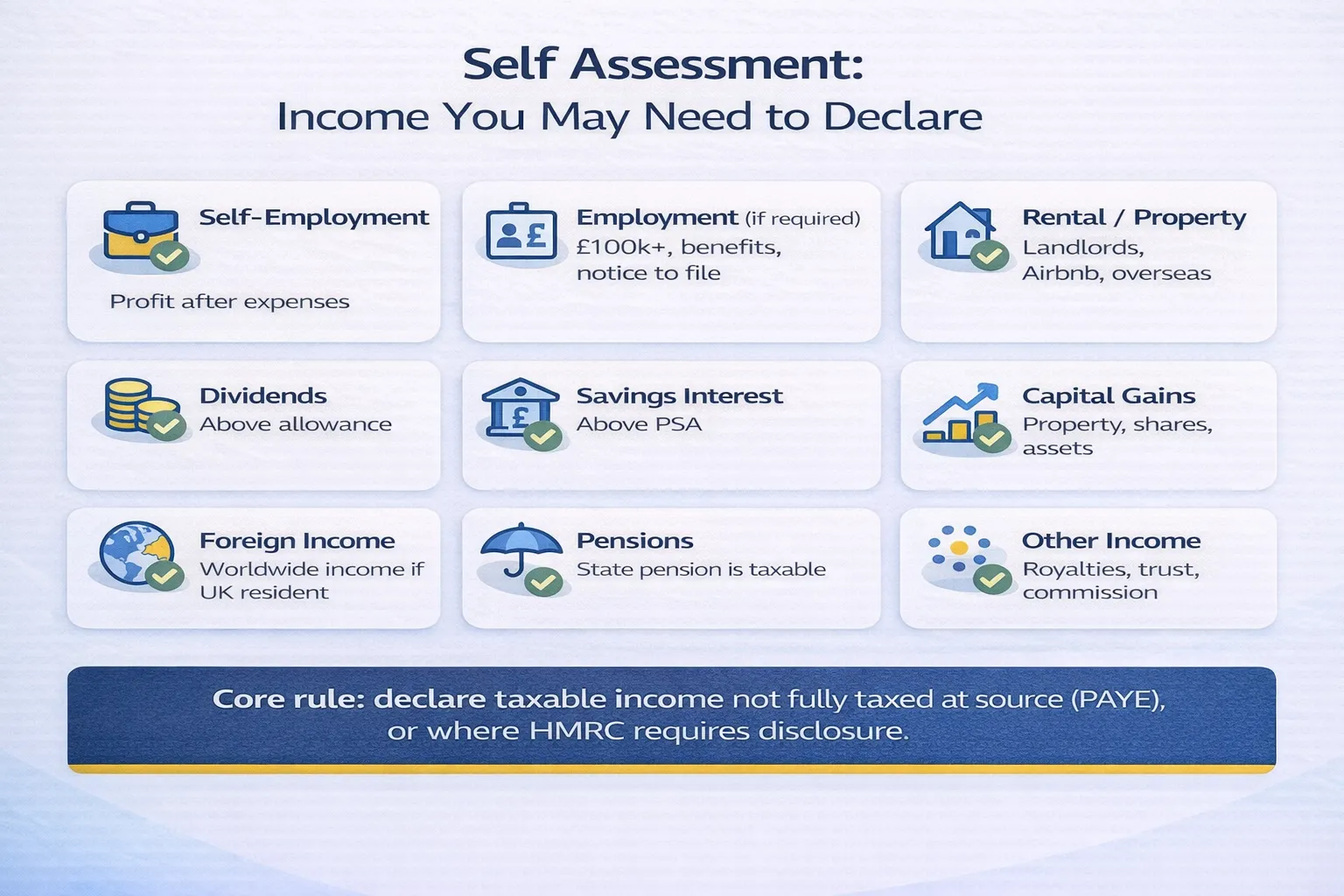

You must declare all taxable income that is not fully taxed at source through PAYE, or where HMRC requires full disclosure.

This typically includes self-employment profits, rental income, dividends above allowances, capital gains, foreign income, and certain pension income.

In this guide, we explain what income must be reported to HM Revenue and Customs (HMRC), so you can stay compliant and avoid penalties.

Official guidance is available here:

https://www.gov.uk/self-assessment-tax-returns

Common Types of Taxable Income to Report

1. Self-Employment Income

If you are self-employed and earn more than £1,000 gross income in a tax year, you will usually need to register and file a Self Assessment tax return.

You must declare:

- Total business income (before expenses)

- Allowable business expenses

- Net profit

Examples include:

- Freelance services

- Consulting

- Contracting

- Online selling (eBay, Amazon, Etsy, etc.)

- Gig economy income

Important: tax is charged on profit, not turnover. However, you must declare the full income figure first, then deduct allowable expenses.

2. Employment Income (When Filing Is Required)

If you are employed under PAYE, tax is normally deducted automatically. However, you may still need to declare employment income if:

- Your total income exceeds £100,000

- You have multiple income sources

- You received benefits in kind (company car, medical insurance)

- HMRC issued a notice to file

Figures are taken from your:

- P60

- P45

- P11D

High earners often need to file because the Personal Allowance reduces once income exceeds £100,000.

3. Rental and Property Income

Landlords must declare rental income when it exceeds reporting thresholds.

You must report:

- Gross rental income

- Allowable expenses (repairs, agent fees, insurance, etc.)

- Net rental profit

This applies to:

- Buy-to-let properties

- Furnished holiday lets

- Overseas property

- Short-term lets (e.g. Airbnb)

Mortgage interest is no longer deducted in full. Instead, it is given as a basic rate tax credit, so accurate reporting is essential.

Investment, Savings, and Asset-Based Income

4. Dividend Income

If you receive dividends from:

- Your limited company

- UK shares

- Overseas investments

You may need to declare them if they exceed the annual dividend allowance.

Dividends are not taxed through PAYE. Even if Corporation Tax has already been paid by the company, dividends are personal income when distributed to you.

5. Savings and Interest Income

Banks do not always deduct tax automatically.

You may need to declare an interest in:

- Savings accounts

- Fixed-term deposits

- Peer-to-peer lending

If your total income exceeds the Personal Savings Allowance, additional tax may be due.

6. Capital Gains

Capital Gains Tax (CGT) applies when you sell certain assets for more than you paid.

You may need to declare gains from:

- Second properties

- Shares and investments

- Business assets

- High-value personal items

Some UK property sales must be reported within 60 days of completion, even before filing your annual return.

Accurate calculation, including allowable costs and exemptions, is essential.

Overseas, Pension, and Miscellaneous Earnings

7. Foreign Income

If you are a UK tax resident, you generally must declare worldwide income.

This includes:

- Overseas employment income

- Foreign rental income

- Offshore bank interest

- Dividends from foreign companies

Special rules apply if claiming the remittance basis.

8. Pension Income

Most private pensions are taxed at source, but you may still need to declare:

- State Pension

- Private pensions

- Overseas pensions

The State Pension is taxable but paid without tax deducted, so it must usually be included.

9. Other Taxable Income

You may also need to declare:

- Partnership income

- Trust distributions

- Royalties

- Commission income

- Casual or one-off earnings

Even relatively small amounts can create reporting obligations depending on your overall income.

Exemptions and Non-Reportable Income

What Income Does NOT Need to Be Declared?

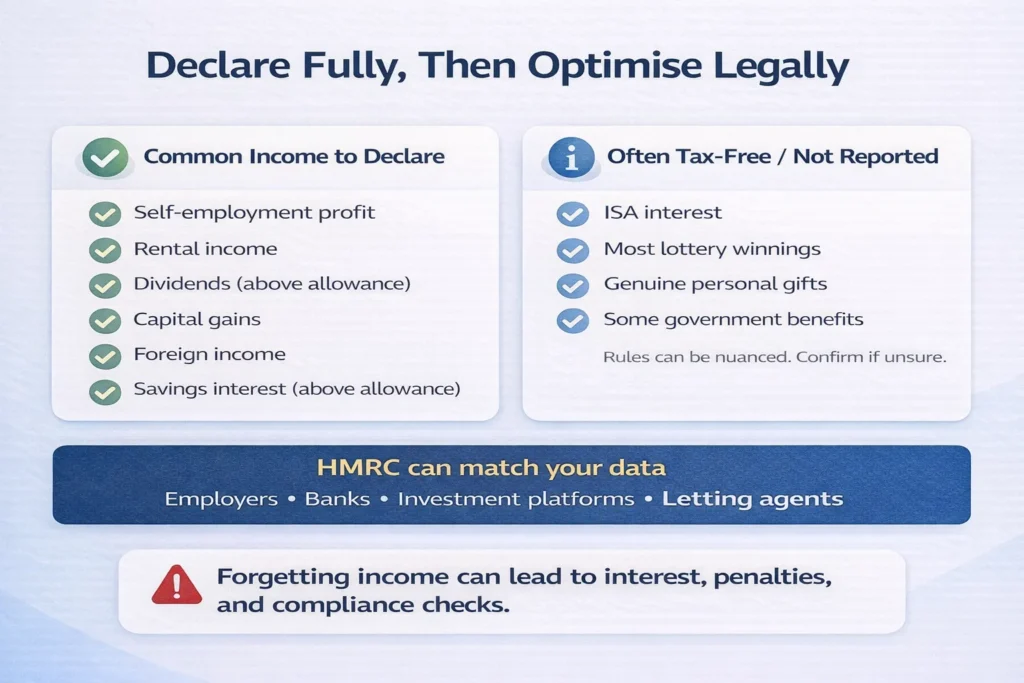

Certain income is typically tax-free and does not require reporting, such as:

- ISA interest

- Most lottery winnings

- Certain government benefits

- Genuine personal gifts

However, tax rules can be nuanced. When in doubt, confirm before assuming.

Compliance and Regulatory Risks

What Happens If You Forget to Declare Income?

HMRC receives data directly from:

- Employers

- Banks

- Investment platforms

- Letting agents

If income is omitted, consequences may include:

- Interest charges

- Financial penalties

- Compliance checks

Penalties depend on whether the omission was careless or deliberate. Voluntary disclosure usually reduces the impact.

The Key Principle: Declare Fully, Then Optimise Legally

The safest approach is:

- Declare all relevant income accurately.

- Claim allowable expenses and reliefs.

- Optimise your tax position within HMRC rules.

Compliance comes first. Structured planning follows.

Summary: Income You Usually Must Declare

You will typically need to report income if it:

- Is not fully taxed through PAYE

- Exceeds HMRC thresholds

- Falls within Self Assessment reporting rules

Common examples include:

- Self-employment income over £1,000

- Rental income

- Dividends above allowance

- Capital gains

- Foreign income

- Earnings over £100,000

Understanding what must be declared helps you stay compliant and avoid unnecessary penalties.

Unsure What to Include?

If you are uncertain whether certain income should be declared or want reassurance that your tax return is accurate, structured professional guidance can provide clarity.

For a compliant income review tailored to your circumstances.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record