A complete guide to Capital Gains Tax on UK property in 2026/27: the 60-day reporting and payment deadline, new rates from April 2026, Private Residence Relief, Business Asset Disposal Relief, and the most common mistakes that trigger HMRC penalties.

Selling a residential property in the UK triggers a chain of reporting obligations that many landlords and homeowners do not fully understand until they have already missed a deadline. The Capital Gains Tax rules for property in 2026/27 involve a 60-day reporting and payment deadline that runs from completion, rates that changed from April 2026, and reliefs that require careful planning to access correctly.

This guide covers the current CGT rates on UK property, the 60-day rule and what happens if you miss it, the reliefs available in 2026/27, and the specific situations — multiple properties, inherited property, separating couples — where professional advice avoids expensive mistakes.

Capital Gains Tax Rates on UK Property in 2026/27

For disposals of UK residential property made on or after 6 April 2026, the CGT rates are:

| Taxpayer | Rate | When It Applies |

|---|---|---|

| Basic rate taxpayer | 18% | On gains that fall within the basic rate income tax band |

| Higher / additional rate taxpayer | 24% | On gains above the basic rate band |

| Trusts and estates | 24% | On most disposals, with annual exemption of £1,500 |

| Business Asset Disposal Relief | 18% | Qualifying business disposals, up to £1m lifetime limit |

Your capital gain is added to your other income when determining the rate — so a basic rate taxpayer with a large gain may find part of it taxed at 24% because the gain pushes them into the higher rate band. The annual exempt amount remains £3,000 for individuals in 2026/27. The first £3,000 of net gains in any tax year is tax-free. This cannot be carried forward and has fallen sharply from £12,300 in 2022/23, making annual planning more important than before.

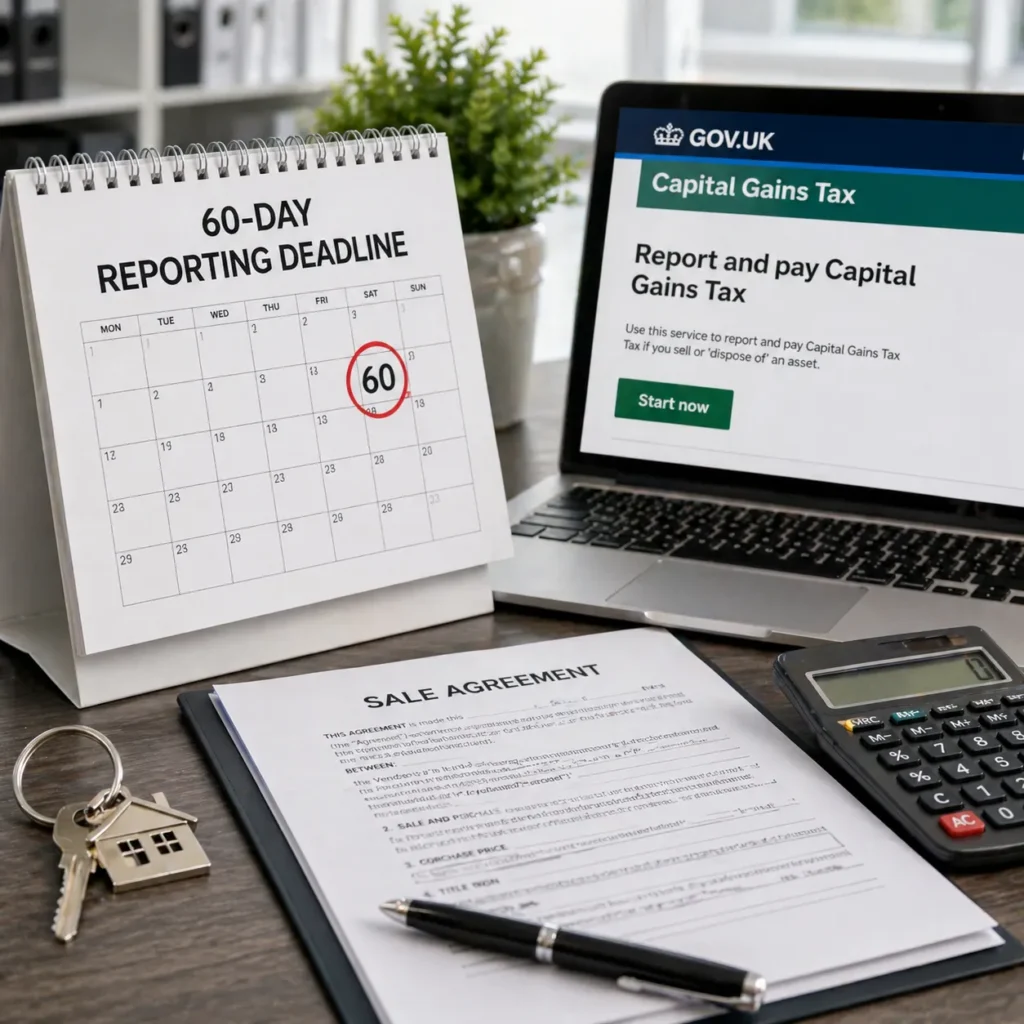

The 60-Day Reporting Rule: What It Is and Why It Catches People Out

When you sell a UK residential property on which Capital Gains Tax is due, you must report the disposal and pay the estimated CGT owed within 60 days of the completion date. This is reported through HMRC’s Capital Gains Tax on UK property account — a separate online system from your Self Assessment return.

⚠️ The 60-Day Clock Starts at Completion

The deadline is calculated from the date of completion, not the date of exchange of contracts. If completion takes place on 1 May 2026, your deadline is 30 June 2026. Conveyancing solicitors do not automatically notify HMRC; that obligation sits with you or your accountant.

When Does the 60-Day Rule Apply?

The rule applies to UK residential property disposals. It does not apply to commercial property, shares, cryptocurrency, or other non-residential assets — those are reported through the annual Self Assessment tax return with a 31 January deadline.

You must file within 60 days even if no tax is due, if your total disposal proceeds for the tax year exceed £50,000 or your total gains (before losses) exceed the £3,000 annual exempt amount. Missing this filing obligation triggers an automatic penalty regardless of whether any CGT is actually payable.

Penalties for Missing the 60-Day Deadline

| How Late | Penalty |

|---|---|

| Day 1–30 late | £100 automatic penalty |

| 3 months late | Daily penalty of £10 per day (up to 90 days) |

| 6 months late | Further penalty: 5% of tax due or £300 (whichever is greater) |

| 12 months late | Further penalty: additional 5% of tax due or £300 |

| Late payment of CGT | Interest at Bank Rate + 2.5% from due date |

Private Residence Relief: When Your Home Sale Is Tax-Free

If you are selling your main home, Private Residence Relief (PRR) usually means no Capital Gains Tax is due. The relief covers the period the property was your main residence plus the final nine months of ownership, even if you were not living there at the point of sale.

PRR becomes more complex in several situations our CGT team regularly handles:

Partial Occupation

If you owned a property for ten years, rented it out for five, then moved in before selling — only the period of actual occupation plus the final nine months qualifies for PRR. The letting period is exposed to CGT. The gain is apportioned on a time basis between the qualifying and non-qualifying periods.

Two Properties — Main Residence Nomination

If you own more than one residential property, you can nominate which is your main residence for CGT purposes. The nomination must be made within two years of acquiring the second property. An unmade or outdated nomination can result in a significantly higher CGT bill on the eventual sale of the wrong property. We review nominations with all clients who acquire a second property as standard.

Letting Relief — Now Restricted

Letting relief, which previously sheltered up to £40,000 of gain, is now restricted to properties where you are in shared occupation with your tenant at the time of disposal. If you let your entire home while you lived elsewhere, letting relief no longer applies. This change has significantly reduced the relief available to former owner-occupier landlords.

Business Asset Disposal Relief in 2026/27

Business Asset Disposal Relief (BADR), formerly Entrepreneurs’ Relief, provides a reduced CGT rate on qualifying business disposals. From 6 April 2026, the BADR rate increased to 18%, up from 14% for disposals from April 2025. The lifetime limit remains £1 million.

Key conditions for BADR to apply:

- You must have owned at least 5% of shares and voting rights for at least two years

- The company must be a qualifying trading company (not an investment company)

- You must have been an officer or employee of the company throughout the two-year period

- You must be disposing of shares, the whole business, or business assets used in the business for the same two-year period

The two-year qualifying period is the most common trap for founders who restructured their shareholding, accepted external investment (which diluted their holding below 5%), or changed their role shortly before a planned sale. Our CGT advisory service reviews BADR eligibility well in advance of any planned disposal.

Inherited Property and CGT

When you inherit a property, the base cost for CGT purposes is the market value at the date of death — the probate value — not the original purchase price paid by the deceased. This is called inheritance uplift.

A property inherited at a value of £350,000 and subsequently sold for £420,000 produces a taxable gain of £70,000 (less selling costs and the annual exempt amount) — not a gain calculated from the price paid decades earlier. For inherited properties the beneficiary does not live in, there is no PRR, the gain is fully exposed to CGT at 18% or 24%, and the 60-day reporting rule applies.

We see a significant number of clients who receive unexpected penalties because they assumed the inherited nature of a disposal changed the filing timeline. It does not. Day 1 of the 60-day clock is the date of completion of the sale.

Couples, Separation, and CGT on Property

Transfers of assets between spouses and civil partners are treated as a no-gain, no-loss transaction — no CGT arises on the transfer itself, provided the couple are living together for at least part of the tax year.

Following the 2023 reforms, a separating couple now has up to three years from the tax year of separation to transfer assets on a no-gain, no-loss basis. Transfers made under a formal court order as part of divorce proceedings continue on a no-gain, no-loss basis with no time limit.

For couples with property portfolios who are separating, this three-year window provides meaningful planning flexibility. Which properties transfer to which party, and in which tax year, can substantially affect the total CGT exposure across the couple. This is an area where early advice produces materially better outcomes than acting under time pressure.

Non-UK Residents Selling UK Property

Non-UK residents disposing of UK residential property are subject to CGT and the 60-day reporting rule in exactly the same way as UK residents. Non-resident CGT rules differ in how the gain is calculated — typically only gains accruing from April 2015 are within scope unless an election is made to use the original purchase price. HMRC actively monitors non-resident disposals. Penalties and interest begin accumulating from day 61 regardless of residence status.

The Seven CGT Mistakes That Cost Property Owners Most

- Missing the 60-day deadline. The most common CGT error for property disposals. Conveyancers do not notify HMRC on your behalf.

- Using the wrong base cost for inherited property. Using the original purchase price rather than the probate value produces an overstated gain and overpayment of CGT.

- Not nominating a main residence for two-property owners. An unreviewed or outdated nomination can result in avoidable CGT on the sale of the wrong property.

- Missing BADR qualifying periods. The two-year rule can be disrupted by shareholding changes, dilution, or role changes that were not flagged as CGT-relevant at the time.

- Not reporting where proceeds exceed £50,000. Even where no CGT is due, disposals with proceeds above £50,000 in a tax year must be reported within 60 days.

- Claiming letting relief incorrectly. Letting relief is only available for periods of shared occupation with your tenant — not for periods where the whole property was let and you lived elsewhere.

- Assuming the CGT annual exemption always applies. The £3,000 annual exempt amount is per individual. For jointly owned property, it applies to each owner’s share of the gain — but it cannot be transferred between spouses for CGT purposes without an actual transfer of the asset.

Selling a Property? Manage the 60-Day Deadline

Our Wimbledon CGT team manages the 60-day reporting as a priority for all residential property disposals. We calculate your gain, apply every available relief, and file with HMRC before the deadline.

Discuss Your Property SaleFrequently Asked Questions

Does the 60-day rule apply if I make no profit on the sale?

You may still need to report within 60 days even if no CGT is due, if your total disposal proceeds exceed £50,000 in the tax year. If a loss is made, reporting the loss within 60 days is good practice — it creates a record of the allowable loss which can be carried forward and set against future gains. Your CGT accountant can confirm whether a 60-day report is required in your specific situation.

How is CGT calculated if I own a property jointly?

For jointly owned property, the gain is split between owners in proportion to their legal ownership (typically 50/50 for married couples or equal co-owners). Each owner’s share of the gain is then assessed against their individual income and annual exempt amount. Married couples and civil partners can adjust the split by executing a Form 17 declaration to reflect actual beneficial ownership if different from the legal split — which can affect the CGT rate that applies to each party’s share.

Can I deduct selling costs from my CGT calculation?

Yes. Allowable selling costs that reduce your CGT gain include estate agent fees, solicitor’s conveyancing fees, and surveyor costs related to the sale. Similarly, capital improvements made to the property during your ownership (extensions, conversions — not routine maintenance) can be added to your base cost, reducing the gain.

What is the CGT annual exempt amount for 2026/27?

£3,000 per individual. The exemption cannot be carried forward or transferred. For the 2026/27 tax year (6 April 2026 to 5 April 2027), you can make £3,000 of net capital gains without paying CGT. For trusts, the annual exempt amount is typically £1,500. The reduction from £12,300 in 2022/23 to £3,000 today makes proactive disposal planning across multiple tax years more important than at any previous time.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record