A complete, practical guide to HMRC’s selection criteria, the Connect AI system, and the key risk factors that put taxpayers under formal scrutiny.

Receiving a letter from HMRC announcing a tax investigation is among the most unsettling experiences for any individual taxpayer or small business owner. In 2026/27, with HMRC’s enforcement budget growing and its AI-powered tools becoming more sophisticated, being investigated is no longer rare; it is an increasingly normal part of the UK tax landscape.

This guide explains exactly what triggers an HMRC tax investigation, how HMRC decides who to target, and what you can do to protect yourself.

What Is an HMRC Tax Investigation?

An HMRC tax investigation, formally called a “tax enquiry”, is a formal review by HM Revenue & Customs (HMRC) to verify that you or your business has paid the correct amount of tax.

It may cover income tax, Corporation Tax, VAT returns, PAYE, Capital Gains Tax, or the Construction Industry Scheme (CIS). The enquiry can relate to a single tax year or span many years of financial history.

Investigations are not always a sign that HMRC suspects deliberate fraud. Many enquiries begin because something on a tax return looks unusual when compared against HMRC’s benchmarks, or because a return was selected at random. However, all investigations require your full attention and a prompt, carefully considered response.

Not every letter from HMRC signals a formal investigation. A routine query about one figure on your return is very different from a full Code of Practice 9 investigation. But all HMRC correspondence deserves careful, timely attention, ignoring even a minor query can escalate the matter considerably.

The Three Types of HMRC Tax Investigation

Understanding which type of investigation HMRC has opened is the first step in knowing how serious the situation is and how to respond appropriately.

| Type | Scope | Typical Duration | Common Trigger |

|---|---|---|---|

| Aspect Enquiry | One specific area of your return (e.g. expenses, dividends, or property income) | 3–6 months | Single discrepancy or unusual figure |

| Full Enquiry | Complete review of all business records and potentially personal finances of directors | 12–18 months+ | Multiple red flags; suspected significant error or evasion |

| Discovery Assessment | HMRC discovers new information suggesting previously undeclared income or tax | Varies — can go back 20 years for fraud | New data from third parties; tip-offs; cross-border information sharing |

A full enquiry is the most demanding. HMRC may request years of bank statements, invoices, purchase ledgers, and personal financial records. A business could realistically have senior staff distracted for more than a year navigating the process.

HMRC’s Connect System: The AI Engine Behind Most Investigations

Before exploring individual triggers, it is essential to understand the system that identifies most of them: HMRC’s Connect platform. Launched in 2010 and continuously upgraded since, Connect is now one of the most powerful data analytics tools operated by any government tax authority in the world.

Connect uses artificial intelligence and advanced algorithms to cross-reference over a billion data items from more than 30 external sources, comparing that information against what individuals and businesses declare on their tax returns. When declared figures do not match what Connect expects, the system flags the case for human review.

What Connect monitors:

- Banks, credit card companies, and payment processors (including PayPal and Stripe)

- Land Registry and property portals, tracking purchases, sales, and rental income

- Companies House, company ownership, director details, and filed accounts

- DVLA, vehicle ownership cross-referenced against declared income

- eBay, Etsy, Amazon, Airbnb, and other online selling platforms

- DWP and government benefits data

- Overseas tax authorities via the Common Reporting Standard (CRS / AEOI)

- Accounting software data submitted via Making Tax Digital (MTD)

- Cryptocurrency platforms, CARF reporting now in force since January 2026, feeding real-time crypto data directly to HMRC

- Social media, monitored in criminal investigation cases with legal oversight

MTD for Income Tax is now live for self-employed individuals and landlords earning above £50,000 (since April 2026), with the threshold dropping to £30,000 in April 2027. HMRC already receives transaction-level accounting data from your software automatically. Any inconsistency between your quarterly updates and your annual return is immediately visible to Connect.

The system deploys predictive modelling, statistical tests including Benford’s Law, and dynamic benchmarking to identify outliers. It can detect whether your car or home’s value is inconsistent with your declared income, whether turnover in your accounting software matches your VAT return, or whether rental property income is hidden by cross-referencing Land Registry records with council tax data.

According to HMRC’s 2026 policy update, the Connect platform contributed £4.6 billion in additional tax revenue in the last financial year. HMRC secured an estimated £48 billion in compliance yield in 2025–26, with investigations up 28% year-on-year and a 91% prosecution success rate for criminal tax cases, and enforcement activity is set to intensify further in 2026/27.

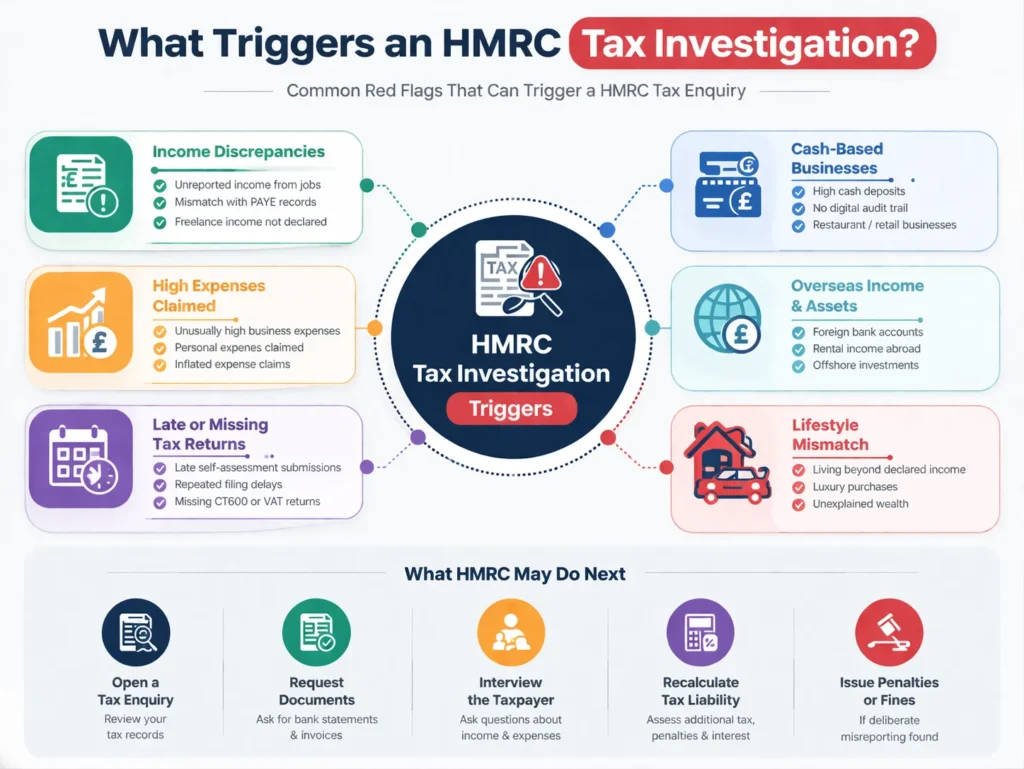

The 12 Main Triggers for an HMRC Tax Investigation

While HMRC does not publish its exact risk-scoring methodology, years of professional experience and data from investigation cases reveal the most consistent red flags. Here are the twelve most significant triggers you need to know about.

- Unexplained Income Fluctuations: Sudden, large changes in declared income between tax years without an obvious business reason are one of Connect’s most reliable signals. A drop from £100,000 to £50,000 in a single year will invite scrutiny.

- Unusually High Expense Claims: HMRC benchmarks your expense ratios against similar businesses in your sector. Claiming a gross profit margin well below the industry average, or consistently claiming high allowable expenses relative to turnover, triggers an immediate flag.

- Late or Amended Returns: Filing Self Assessment, VAT, PAYE, or Corporation Tax returns consistently late signals poor record-keeping. Frequently amending returns after submission is equally concerning; it suggests figures were not accurate to begin with.

- Persistent Business Losses: Every business can have a bad year. But consistently reporting losses over several years while continuing to trade prompts HMRC to question whether expenses are being inflated or all income is being declared.

- Lifestyle Inconsistent With Income: If your declared income cannot reasonably support the assets you own, a second property, a premium car, overseas travel, Connect will flag the mismatch. This is HMRC’s ‘lifestyle v. income’ check.

- Cash-Heavy Business Operations: Restaurants, takeaways, hairdressers, taxi firms, and market traders face heightened scrutiny because cash is harder to trace. HMRC applies specific benchmarks to cash businesses and watches for bank deposits exceeding declared revenue.

- Third-Party Tip-Offs: HMRC operates an anonymous tip-off line. Reports from disgruntled ex-employees, former business partners, or competitors can open a targeted investigation, regardless of whether the information is accurate.

- Overseas Income or Assets: The Common Reporting Standard means foreign banks share UK residents’ account data with HMRC automatically. Undeclared offshore income or foreign property is one of the highest-yield areas for HMRC investigation.

- CIS Scheme Non-Compliance: Construction businesses subject to CIS must verify subcontractors and deduct tax correctly. Errors in CIS returns or unregistered subcontractors frequently trigger enquiries across the sector.

- R&D Tax Credit Claims: As of 2026/27, HMRC’s R&D Anti Abuse Unit operates a full volume compliance model. An estimated 17–20% of all R&D claims are being flagged for enquiry, a level of scrutiny that is only increasing as HMRC recovers billions in overclaimed relief.

- Online Selling & Gig Economy: Income from eBay, Etsy, Airbnb, Deliveroo, Uber, and similar platforms is now shared with HMRC. If you earn regularly from these sources without declaring it, Connect will almost certainly find it.

- Random Selection: Approximately 7% of all HMRC investigations are entirely random. Even a meticulous taxpayer can be selected, which is why following proper record keeping rules at all times is essential.

A client unknowingly failed to declare rental income from a second property. HMRC discovered it through a combination of Land Registry and council tax data, they knew he wasn’t living there and correctly assumed it was being rented out. He received a letter inviting voluntary disclosure. The case was resolved with a full disclosure of five years of records, with penalties significantly lower than they would have been had HMRC opened a formal investigation unprompted.

High-Risk Industries Under Increased HMRC Scrutiny

Certain industries face above-average investigation rates, not necessarily because businesses in those sectors are dishonest, but because the nature of the business creates a higher statistical likelihood of errors or non-compliance.

Industries currently under heightened HMRC focus:

- Restaurants, takeaways, pubs, and hospitality (cash transactions, VAT compliance)

- Construction and trades (CIS scheme compliance, subcontractor verification)

- Hair and beauty salons, barbers, and therapists (cash-heavy, informal payments)

- Retail and market stalls (point-of-sale income, stock discrepancies)

- Taxis, private hire, and couriers (platform income, mileage claims)

- Landlords and property investors (rental income, allowable expenses, CGT)

- IT contractors and consultants (IR35 / off-payroll working rules)

- Social media influencers and content creators (undeclared sponsorship and brand income)

- R&D tax credit claimants (17–20% of claims now being flagged for enquiry)

- Cryptocurrency traders and investors (CARF now in effect, exchanges sharing data with HMRC in 2026/27)

If your business operates in one of these sectors, meticulous record-keeping is not optional; it is your primary defence. HMRC’s benchmarking data for these industries is detailed, and deviating from expected norms without a clear documented reason will attract attention.

What Triggers HMRC Investigations for Individuals?

Individuals, including employees, landlords, retirees, and investors, are not immune to HMRC scrutiny. Several specific circumstances commonly lead to enquiries into personal tax affairs.

Undeclared Rental Income

HMRC cross-references Land Registry records, council tax data, and information from letting agencies. If you own a property you are not living in, HMRC may already assume it is generating rental income. The Let Property Campaign offers a route to voluntary disclosure, which typically results in significantly lower penalties than a formal investigation.

Capital Gains Tax Omissions

Selling a second property, shares, or other assets without reporting the gain is a common trigger. Conveyancing solicitors and estate agents share property transaction data with HMRC, and Connect cross-references this against CGT returns automatically.

Multiple Income Sources Not Declared

A full-time employee with a freelance side income, income from an online shop, or earnings from short-term lets who fails to register for a Self Assessment tax return is highly visible to Connect. HMRC receives data from payment processors, platforms, and banks that makes these income streams traceable.

IR35 and Off-Payroll Working

IT contractors and consultants operating through personal service companies remain a priority for HMRC compliance teams. If your working arrangements resemble employment rather than genuine self-employment, you may be inside IR35, and HMRC will pursue the relevant unpaid income tax and National Insurance.

One widely cited case involved a client who claimed exactly £9,999 in miscellaneous expenses for three consecutive years, just under the threshold that might attract attention. The extreme consistency of the figure itself became a red flag for HMRC’s pattern-recognition tools. Always ensure your figures reflect genuine business activity, not a convenient round number.

What Happens During an HMRC Tax Investigation?

If HMRC opens an enquiry, the process typically follows a defined sequence. Understanding it helps you respond correctly and avoid inadvertently making matters worse.

| Step | What Happens | Your Action |

|---|---|---|

| 1. Enquiry Letter | HMRC sends a formal letter under Section 9A (Self Assessment) or Section 12AC (partnerships). You normally have 30 days to respond. | HMRC requests records, bank statements, invoices, receipts, payroll records, and business accounts, sometimes covering several years. |

| 2. Information Requests | HMRC requests records, bank statements, invoices, receipts, payroll records, business accounts, sometimes covering several years. | Gather all requested documents systematically. Your adviser can help identify what is and is not required. |

| 3. Meetings | HMRC may request a meeting at your premises, your accountant’s office, or an HMRC office. | You are entitled to have your accountant represent you. Never attend an HMRC meeting without professional support. |

| 4. Findings & Assessment | HMRC issues its conclusions. Additional tax may be assessed. Penalties depend on whether errors were innocent, careless, or deliberate. | Review the findings carefully with your adviser. Penalties for innocent errors are significantly lower. |

| 5. Appeal or Settlement | You have the right to appeal to the First-tier Tax Tribunal. In many cases, a negotiated settlement is reached before this stage. | Experienced representation significantly improves settlement outcomes and can reduce penalty amounts. |

How Far Back Can HMRC Investigate?

The look-back period for an HMRC investigation depends on the nature of any error, and the consequences increase significantly for deliberate non-compliance.

| Circumstances | Maximum Look-Back Period |

|---|---|

| Innocent mistake or careless error | 4 years from the end of the relevant tax year |

| Careless but not deliberate understatement | 6 years |

| Deliberate understatement (no fraud) | 20 years |

| Deliberate tax fraud | 20 years, and potential criminal prosecution with no time limit |

The longer the investigation period, the more significant the potential liability, because HMRC charges interest on all unpaid tax going back to when it was originally due. For a serious case, interest charges alone can substantially exceed the original tax owed.

How to Reduce Your Risk of an HMRC Investigation

No individual or business can entirely eliminate the possibility of an HMRC enquiry; the random selection element alone ensures that. But the overwhelming majority of triggered investigations arise from identifiable risk factors that can be managed with professional support.

- File all returns, Self Assessment, VAT, PAYE, and Corporation Tax accurately and on time, every time. Consistent compliance helps you avoid late penalties and reduces your risk profile.

- Keep thorough, well-organised records for at least six years, including invoices, receipts, bank statements, and payroll records.

- Declare all income, including rental income, freelance earnings, online sales, director dividends, and cryptocurrency gains.

- Ensure all expense claims are genuinely ‘wholly and exclusively’ for business purposes. Be especially careful with home office costs, vehicles, and entertainment expenses.

- Document the reason for any significant year-on-year changes in income or expenditure clearly in your records and accounts.

- Enrol in Making Tax Digital for VAT and prepare for MTD for Income Tax, now live from April 2026 for those earning above £50,000. Real-time digital records reduce discrepancies that trigger Connect.

- If you operate in a high-risk sector or claim R&D relief, commission a professional pre-filing review each year before submitting.

- Consider tax investigation insurance, which covers professional fees if you are selected for enquiry.

- If you receive any unexpected HMRC letter, contact a qualified tax adviser before responding. Your initial response can set the tone for the entire investigation.

If you believe you have made errors in previous returns, whether through oversight or genuine mistakes, HMRC offers voluntary disclosure facilities including the Let Property Campaign and the Worldwide Disclosure Facility. Voluntary disclosure consistently results in lower penalties than waiting for HMRC to find the problem first. Protax Consultants can guide you through any disclosure process confidentially.

Frequently Asked Questions (FAQs)

What are the most common triggers for an HMRC tax investigation?

The most common triggers include unexplained income discrepancies flagged by the Connect system, late or amended tax returns, unusually high expense claims relative to turnover, operating in a cash-heavy industry, tip-offs from third parties, and lifestyle inconsistencies with declared income.

How does HMRC decide who to investigate?

HMRC uses its Connect AI platform to cross-reference over a billion data points from banks, Land Registry, Companies House, online marketplaces, and overseas tax authorities. When data does not align with your declared return, Connect flags your case for review. HMRC also acts on tip-offs and selects approximately 7% of cases entirely at random.

Can HMRC investigate you for no reason?

Yes. Approximately 7% of all HMRC investigations are random checks with no specific trigger. Even the most meticulous taxpayer can be selected. This is exactly why maintaining clean, well-organised records at all times is so important.

Will HMRC investigate me if I make an honest mistake on my tax return?

Possibly, but honest mistakes are treated very differently from deliberate evasion. For innocent errors, HMRC can only go back four years, penalties are usually minimal, and the matter is often resolved quickly. The key is to respond promptly and make a voluntary disclosure before HMRC contacts you.

What should I do if I receive an HMRC investigation letter?

Do not ignore the letter. Do not respond to HMRC directly before speaking to a qualified accountant or tax adviser. You normally have 30 days to respond. An experienced professional can help you gather the correct records, communicate appropriately with HMRC, and significantly reduce any potential penalties.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record