Filing your first Self Assessment tax return can feel overwhelming. If you’re newlyself-employed, earning rental income, or making money from a side hustle, you may not know where to start.

The good news is that the process is structured and manageable once you understand the steps.

This guide explains exactly what to do, when to do it, and how to stay compliant with UK tax rules, calmly and confidently.

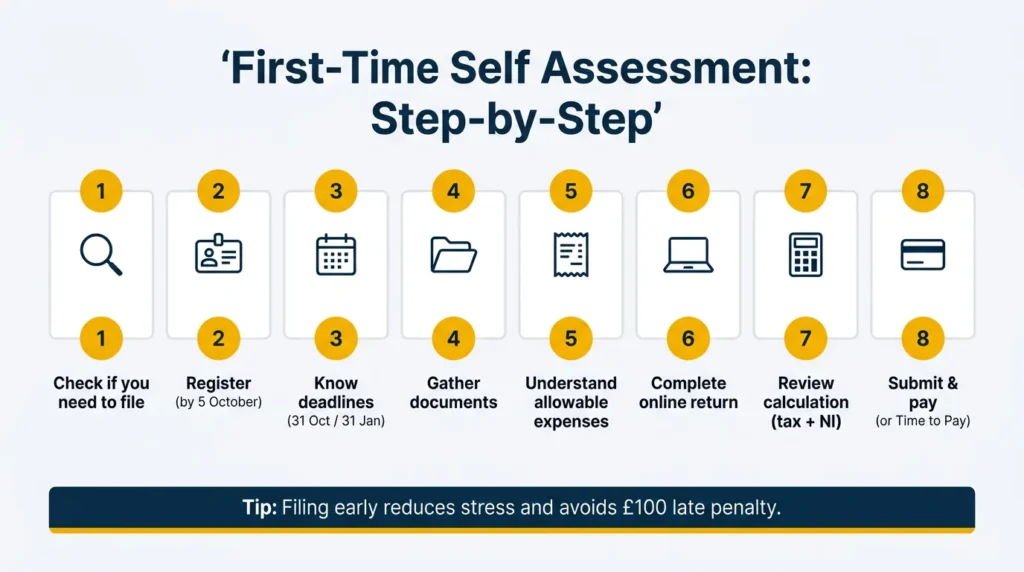

Step 1: Check If You Need to File

Before anything else, confirm whether filing is required.

You generally need to file a Self Assessment tax return if you:

- Are self-employed and earned more than £1,000 (gross)

- Have rental income above reporting thresholds

- Earn over £100,000 per year

- Receive untaxed income (dividends, foreign income, etc.)

- Made taxable capital gains

The system is administered by HM Revenue and Customs (HMRC).

You can check the official criteria here

If unsure, verify rather than assume.

Step 2: Register for Self Assessment

If this is your first time, you must register before filing.

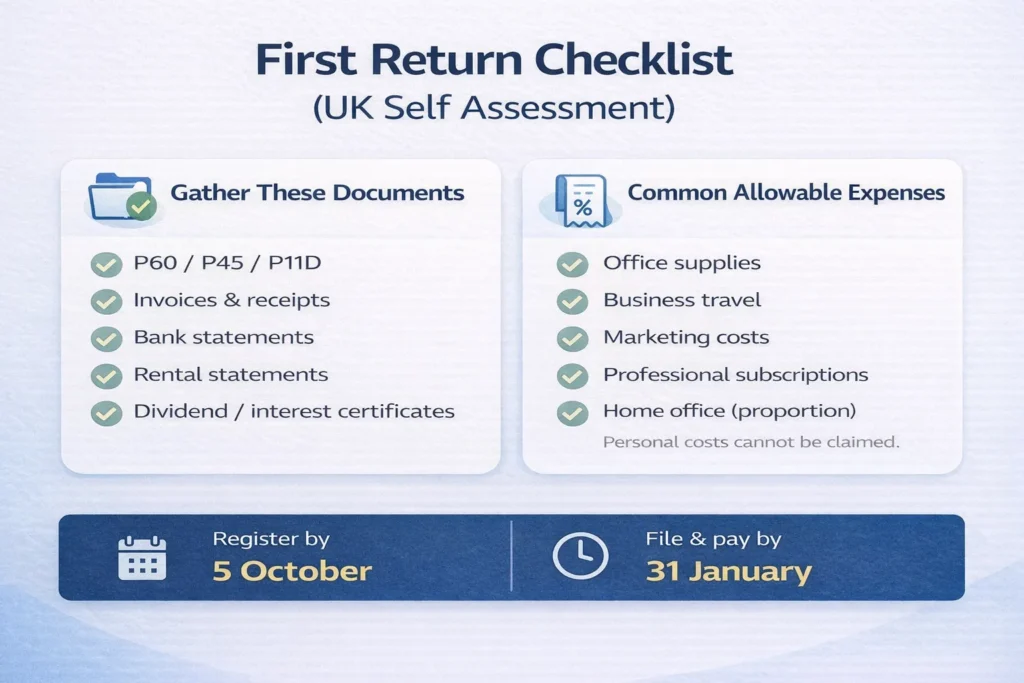

Registration Deadline

You must register by 5 October following the end of the tax year in which you became liable.

For example, if you started freelancing in July 2025 (tax year 2025–26), you must register by 5 October 2026.

After Registration

HMRC will send you:

- A Unique Taxpayer Reference (UTR)

- Online account activation details

Keep your UTR safe, you’ll use it every year.

Step 3: Know the Key Deadlines

There are two main deadlines:

- 31 October – Paper return deadline

- 31 January – Online filing deadline and payment due date

Most first-time filers choose online submission, as it provides confirmation and automatic tax calculations.

Missing the deadline results in an automatic £100 penalty, even if no tax is owed.

Step 4: Gather Your Documents

Preparation makes everything easier. Collect:

Employment Income

- P60 or P45

- P11D (if applicable)

Self-Employment Records

- Sales invoices

- Expense receipts

- Bank statements

Other Income

- Rental statements

- Dividend vouchers

- Interest statements

Good record keeping reduces stress and errors.

Step 5: Understand Allowable Expenses

If you are self-employed, you are taxed on profit, not turnover.

Common allowable expenses include:

- Office supplies

- Business travel

- Professional subscriptions

- Marketing costs

- A proportion of home office expenses

Personal costs cannot be claimed.

Correctly identifying allowable expenses improves tax efficiency while staying compliant.

Step 6: Complete the Online Return

Log in to your HMRC account and complete the return section by section.

You’ll declare:

- Employment income

- Self-employment income

- Property income

- Capital gains

- Pension contributions

- Student loan repayments

The system calculates your tax automatically once all information is entered.

Take your time and review carefully before submission.

Step 7: Review the Tax Calculation

After completing the form, you’ll see:

- Total tax due

- National Insurance contributions

- Any payments on account

Payments on account are advance payments toward next year’s bill and apply if your tax exceeds certain thresholds.

Understanding this prevents unexpected payment demands.

Step 8: Submit and Pay

Once submitted, you’ll receive confirmation.

Payment methods include:

- Bank transfer

- Debit card

- Direct Debit

- Time to Pay arrangement (if eligible)

Payment is due by 31 January.

If you cannot pay in full, contact HMRC promptly to discuss instalments. Ignoring the issue leads to interest and further penalties.

Common Mistakes First-Time Filers Make

Avoid these common errors:

1. Leaving It Until January

January is the busiest month. Filing early reduces stress and allows time to correct mistakes.

2. Confusing Revenue with Profit

Tax applies to profit after expenses.

3. Forgetting Additional Income

Even a small side income over £1,000 must be declared.

4. Not Budgeting for Tax

Set aside a percentage of income throughout the year to avoid cash flow pressure.

Do You Need an Accountant for Your First Return?

Not everyone does.

If your income is straightforward, filing yourself may be manageable.

Professional guidance may be helpful if you:

- Have multiple income sources

- Earn over £100,000

- Own rental property

- Are unsure about allowable expenses

- Want reassurance that your return is correct

The goal is compliance and clarity, not aggressive tax strategies.

What Happens After You File?

Once submitted:

- Keep records for at least 5 years

- Prepare for potential July payments on account

- Continue tracking income and expenses for the next tax year

Self-assessment becomes easier after the first year, as the process becomes familiar.

Final Thoughts

Filing your first Self Assessment tax return may seem daunting, but it follows a clear structure.

In summary:

- Confirm you need to file

- Register before 5 October

- Prepare accurate records

- Submit online before 31 January

- Pay on time or arrange instalments

Acting early reduces uncertainty and prevents penalties.

Need Reassurance?

If you’re filing for the first time and want peace of mind that everything is correct, structured guidance can help clarify your obligations.For tailored support, contact Protax Consultants