The UK tax system is currently seeing its most significant change in a generation. Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA) is HM Revenue and Customs’ plan to move tax reporting into the modern age.

From April 2026, the way many self-employed people and landlords report their earnings will change forever. Instead of one annual deadline, you will move to a digital system of regular updates. This major shift aims to make taxes easier and more accurate, but it requires careful preparation now to ensure a smooth transition.

What is Making Tax Digital for Income Tax?

Making Tax Digital is a government scheme designed to make tax filing more accurate and easier to manage. It moves away from paper-based records and manual spreadsheets toward approved HMRC-compatible software.

If you already pay VAT, you may be familiar with MTD. The next phase brings these digital rules directly to Income Tax.

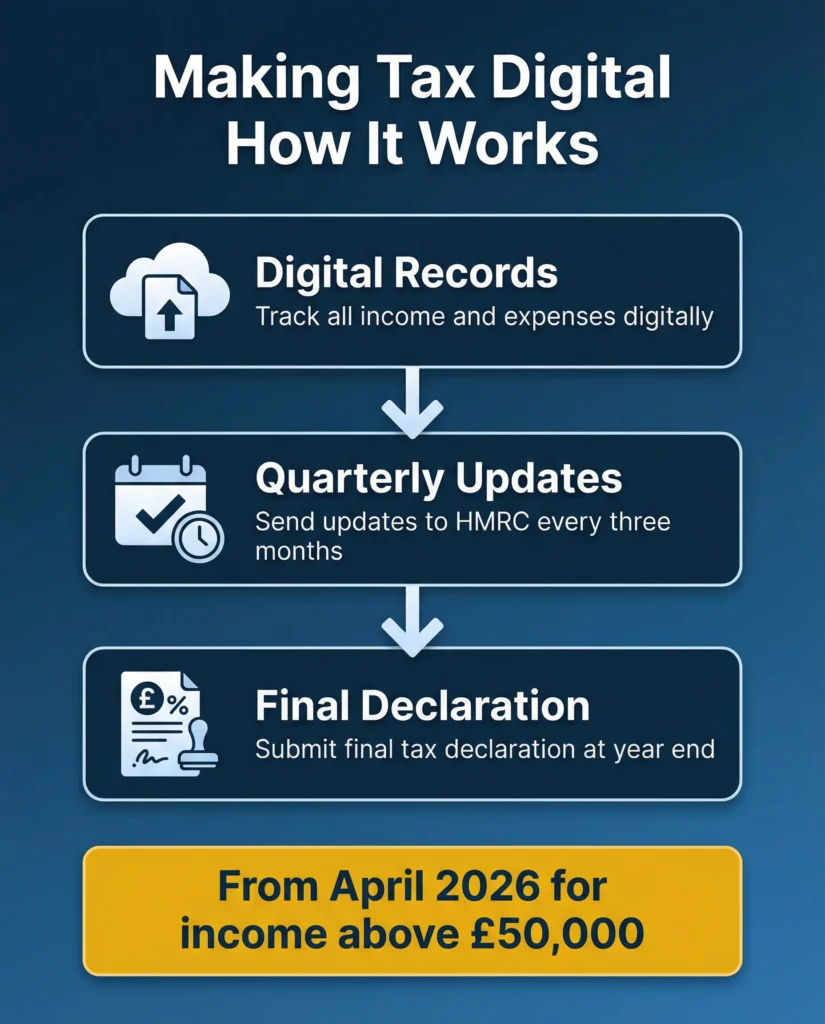

The Big Shift: From Annual to Quarterly Updates

Under the old system, you likely submitted one single Self Assessment tax return per year.

Under MTD, the process changes. You will now:

- Keep digital records of every transaction.

- Send quarterly updates (every three months) to HMRC.

- Submit a final declaration at the end of the tax year.

Who is Affected by the April 2026 Changes?

Not everyone has to join the new system at once. The rollout depends on exactly how much you earn from self-employment or property:

- April 2026: Self-employed individuals and landlords earning over £50,000.

- April 2027: Self-employed individuals and landlords earning over £30,000.

Note: Your “income” refers to your total gross turnover (all the money coming into your business), not just your final profit.

Key Requirements Under the New Rules

To stay compliant with HMRC, you must follow three main steps once you join the MTD scheme:

1. Digital Record Keeping

You can no longer keep your receipts in a shoebox or record them in a paper ledger. You must follow strict self-assessment record rules and record all income and expenses digitally. Most people find that using dedicated accounting software is the easiest way to do this.

2. Quarterly Updates

Every three months, you must send a summary of your business’s income and spending to HMRC through your software. This gives you a clearer, real-time view of how much tax you owe throughout the year. Knowing your estimated tax bill in advance helps you avoid Self Assessment penalties caused by unexpected January bills.

3. End of Period Statement (Final Declaration)

At the end of the tax year, you will finalise your figures and submit a final declaration. This replaces the traditional Self Assessment tax return and allows you to claim any tax reliefs, allowances, or personal adjustments.

The Benefits of Going Digital

While a brand-new system can feel daunting, there are clear advantages to making the switch:

- Fewer Mistakes: Software helps catch basic errors that often happen with manual entry.

- Real-Time View: You can see exactly how your business is performing financially at any time.

- Better Budgeting: By seeing your estimated tax bill grow each quarter, you can safely set aside the right amount of money.

- Faster Processes: Linking your software directly to your business bank account can completely automate your book-keeping.

How to Prepare Your Business Now

April 2026 may seem far away, but setting up your digital systems now will prevent a stressful, last-minute rush.

- Check Your Income: Look at your previous tax returns to see if your turnover sits above the £50,000 or £30,000 thresholds.

- Ditch the Paper: If you still use paper records, start moving your data into a digital format today.

- Find Compatible Software: Ensure the software you choose is officially “HMRC-compatible.” This means it can communicate directly with HMRC’s systems.

- Speak to an Accountant: With the new UK tax year approaching, legal and financial experts can help you structure your business correctly and ensure you are ready to meet your new digital obligations.

Summary

The move to Making Tax Digital in April 2026 is mandatory for those earning over £50,000. By embracing digital tools early, you can simplify your relationship with HMRC, reduce paperwork, and gain much better control over your business finances.

Frequently Asked Questions (FAQs)

1. Does the £50,000 threshold refer to profit or turnover?

The threshold is based on your gross income (turnover), not your profit. If your total income from self-employment and property is over £50,000 before you deduct expenses, you must follow MTD rules from April 2026.

2. What if I earn money from both self-employment and rent?

You must combine both income streams to see if you meet the threshold. For example, if you earn £30,000 from a freelance business and £25,000 from rental property (as explained in our landlord Self Assessment guide), your total combined income is £55,000. You would be required to join MTD in April 2026.

3. Do I still need to file a Self Assessment tax return?

The traditional annual Self Assessment tax return is being replaced by the “Final Declaration.” While the name is changing, the deadline remains the same: you must finalise your tax position and pay any tax owed by 31 January following the end of the tax year.

4. Can I still use spreadsheets for my bookkeeping?

Yes, but with a catch. You can use spreadsheets to keep your records, but you must use “bridging software” to send the data to HMRC. You cannot simply email a spreadsheet to HMRC or upload it to their website; the link between your data and HMRC must be strictly digital.

5. Are there any exemptions for people who aren’t “tech-savvy”?

HMRC offers exemptions for those who are “digitally excluded.” This may apply if you cannot use digital tools due to age, disability, a remote location (poor internet), or religious beliefs. You must apply to HMRC directly to be granted this exemption.

6. When are the quarterly deadlines for MTD?

The standard quarterly periods follow the standard tax year:

- Quarter 1: 6 April – 5 July (Deadline: 7 August)

- Quarter 2: 6 July – 5 October (Deadline: 7 November)

- Quarter 3: 6 October – 5 January (Deadline: 7 February)

- Quarter 4: 6 January – 5 April (Deadline: 7 May)

7. Will I get fined if I make a mistake on a quarterly update?

HMRC has confirmed a “soft landing” for penalties starting in April 2026. You will not receive penalty points for late submissions of your first four quarterly updates. However, deliberate errors or failing to keep digital records can still lead to fines.

8. Do I need a separate bank account for my business?

While not legally required for sole traders, it is highly recommended. Using a separate account makes it much easier to link your bank feed to accounting software, which automates your record-keeping and ensures you do not miss claiming any allowable expenses.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record