As we move through the 2025/26 tax year, UK landlords are facing a major turning point in how they manage their finances. Not only do you need to report your current rental income accurately, but you must also prepare for the mandatory shift to digital tax reporting. This upcoming change will permanently alter how property investors communicate with HM Revenue & Customs (HMRC).

This guide covers the current tax rules and the essential steps you must take to ensure your rental business is fully prepared for the new digital era.

What Counts as Rental Income in 2025/26?

HMRC treats your rental activity as a “property business.” You must report all income connected to the property. As explained in our comprehensive landlord Self Assessment guide, taxable income is not just the monthly rent cheque.

You must declare:

- Standard monthly rent from your tenants.

- Service charges for parking or property maintenance.

- Cleaning or utility fees paid by the tenant to you.

- Retained deposits (if you keep a deposit at the end of a tenancy to cover damages).

Key Tax Thresholds and Rates (2025/26)

For the new UK tax year, your rental profit is added to your other income (such as your salary) to determine your final tax band. For most of the UK (excluding Scotland), your profit is taxed at these rates:

- Personal Allowance: Up to £12,570 (0% tax)

- Basic Rate: £12,571 to £50,270 (20% tax)

- Higher Rate: £50,271 to £125,140 (40% tax)

- Additional Rate: Over £125,140 (45% tax)

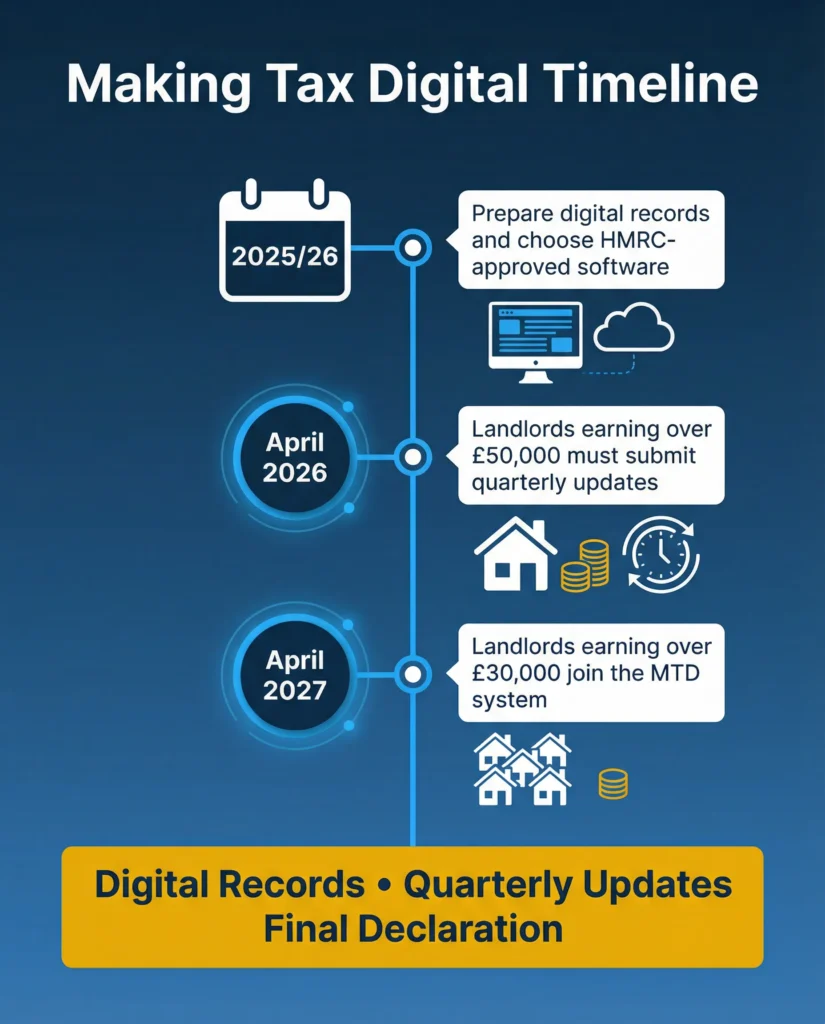

Making Tax Digital: The April 2026 Deadline

The biggest tax change in a generation arrives on 6 April 2026. If your total gross income from self-employment and property is over £50,000, you will no longer file a single annual tax return.

From April 2026, you must:

- Follow strict self-assessment record rules and keep digital records of every transaction.

- Submit quarterly updates to HMRC (every three months).

- Submit a Final Declaration by 31 January to finish the tax year.

Note: If you earn between £30,000 and £50,000, you will join the MTD scheme one year later, in April 2027.

Allowable Expenses: Reducing Your Tax Bill

You only pay tax on your actual profit. This means you can legally subtract specific allowable expenses from your gross income.

Common deductible costs include:

- Repairs and property maintenance (but not capital improvements or extensions).

- Letting agent fees and advertising costs.

- Landlord insurance and professional accounting fees.

- Ground rent and service charges.

A Note on Mortgage Interest (Section 24)

You can no longer deduct your monthly mortgage interest payments directly from your rental income to lower your tax band. Instead, you receive a 20% basic-rate tax credit on these finance costs.

For higher-rate taxpayers, this remains a high cost. As a result, many property owners now seek professional landlord property tax advice to see if moving properties into a Limited Company is more tax-efficient.

Selling Property: Capital Gains Tax (CGT)

If you sell a rental property in the 2025/26 tax year, you may owe Capital Gains Tax on the profit you make.

- Annual Exempt Amount: The first £3,000 of your gain is completely tax-free.

- Basic Rate Taxpayers: You pay 18% on the remaining gain.

- Higher/Additional Rate Taxpayers: You pay 24% on the remaining gain.

The 60-Day Rule: You must report the sale and pay any CGT owed to HMRC within 60 days of the completion date. Missing this strict deadline will result in immediate fines, so prompt reporting is vital to avoid Self Assessment penalties.

How to Prepare for the New Rules Today

Do not wait until the last minute to get your finances in order. Take these steps today:

- Check your 2024/25 records: HMRC uses your income from the tax year that just ended to decide if you must join MTD in April 2026.

- Software Check: Stop using paper receipts or basic spreadsheets. Switch to HMRC-approved software now so you are entirely comfortable using it before it becomes legally mandatory.

Review Ownership: With tax rates and rules changing, speak to an accountant to ensure your current ownership structure is still protecting your wealth.

Frequently Asked Questions (FAQs)

1. Why is my 2024/25 income important for the 2026 MTD deadline?

HMRC looks at your “Qualifying Income” from your most recently filed tax return to determine if you meet the MTD threshold. For the April 2026 rollout, they will look closely at your 2024/25 return.

2. Can I still use Excel for my 2025/26 records?

You can, but for the next tax year (2026/27), you will need special “bridging software” to link that Excel sheet directly to HMRC. It is usually much simpler and safer to switch to a dedicated accounting app right now.

3. What happens if I miss the 60-day CGT deadline?

If you sell a residential property and do not report it to HMRC within 60 days of completion, you will face an immediate £100 penalty, plus daily interest on the unpaid tax. This is entirely separate from your annual Self Assessment.

4. Is the £50,000 MTD threshold based on my profit?

No. The threshold is based on your gross turnover. This is the total amount of rent collected before you pay any bills, mortgage costs, or expenses.

5. I have multiple rental properties. Is the £50,000 limit per property?

No, it applies to your total combined income. For example, if you have three properties that each earn £18,000 a year in rent, your total gross income is £54,000. This means you must join Making Tax Digital in April 2026.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record