A complete 2026/27 guide for UK limited company directors covering the 19% and 25% Corporation Tax rates, how marginal relief works, when your CT600 must be filed, when you must pay, and the most effective legal ways to reduce your company’s tax bill.

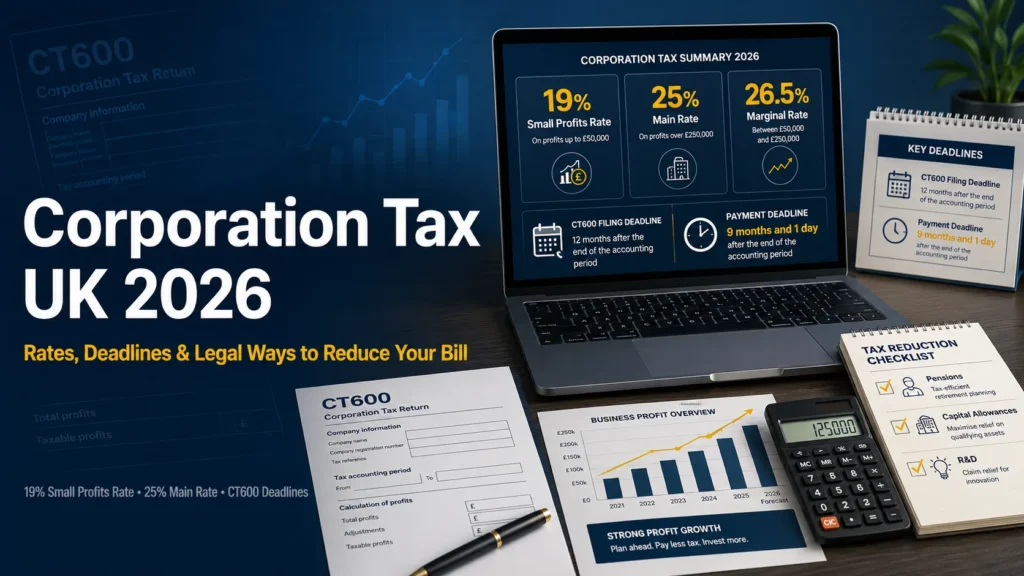

Corporation Tax is the tax your limited company pays on its taxable profits. For the vast majority of small UK companies, the rate structure has remained unchanged since April 2023 and continues into 2026/27: 19% on profits up to £50,000, 25% on profits above £250,000, and an effective rate of 26.5% on profits in the band between the two thresholds. Understanding how these rates interact, when you must pay, and what reliefs are available is essential for every director running a limited company.

Corporation Tax Rates for 2026/27

| Profit Level | Rate | Notes |

|---|---|---|

| Up to £50,000 | 19% (small profits rate) | Full small profits rate applies |

| £50,001 to £250,000 | 19%–25% (marginal relief band) | Effective marginal rate of 26.5% on profits within this band |

| Above £250,000 | 25% (main rate) | Full main rate applies |

These thresholds are for a company with no associated companies. If your company has one or more associated companies (broadly, companies under common control), the thresholds are divided between them. A company with two associated companies, for example, applies the small profits rate to profits up to £16,667 and the main rate above £83,333.

The 26.5% Marginal Rate: The Number Most Directors Miss

The most widely misunderstood feature of the UK Corporation Tax system is the effective marginal rate in the £50,000 to £250,000 band. Most articles simply say “marginal relief applies” and leave it there. In practice, every additional pound of profit within this band is taxed at an effective rate of 26.5%, which is higher than the 25% main rate.

This happens because marginal relief withdraws the benefit of the lower 19% rate as profits increase. Technically, the company is first charged at the full 25% main rate, then a marginal relief fraction (3/200) reduces the bill. The structure of this relief means that each additional £1 of profit within the band costs 25p in main rate tax plus withdraws 1.5p of marginal relief, totalling 26.5p of effective tax on that pound of profit.

⚠️ The Marginal Band Is More Expensive Per Pound Than the Main Rate

If your company’s profits sit between £50,000 and £250,000, every additional pound of profit costs you 26.5p in Corporation Tax, not 25p. This makes pension contributions, capital expenditure timing, and salary adjustments particularly valuable if your profits are in or near this band. A director pension contribution that brings profits from £80,000 to £45,000, for example, saves tax at 26.5% on the £30,000 in the marginal band, plus 19% on the remaining £5,000 reduction, a total saving well above what a flat 25% calculation would suggest.

Corporation Tax Payment Deadlines

For most small and medium-sized companies, Corporation Tax is due 9 months and 1 day after the end of the accounting period. The CT600 tax return must be filed within 12 months of the accounting period end.

| Accounting Period End | CT600 Filing Deadline | Tax Payment Deadline |

|---|---|---|

| 31 March 2026 | 31 March 2027 | 1 January 2027 |

| 30 April 2026 | 30 April 2027 | 1 February 2027 |

| 31 May 2026 | 31 May 2027 | 1 March 2027 |

| 31 December 2026 | 31 December 2027 | 1 October 2027 |

Note that the payment deadline is before the filing deadline. This means you need to calculate your Corporation Tax liability and pay it three months before your CT600 return is due. Many directors are caught out by this: the tax must be paid even before the accounts are formally filed. Penalties for late payment include interest from the due date and percentage-based surcharges on unpaid amounts.

Late Filing Penalties

- 1 day late: £100 automatic penalty

- 3 months late: Further £100 penalty

- 6 months late: HMRC estimates the CT liability and charges 10% of the unpaid tax

- 12 months late: A further 10% penalty on unpaid tax

How to Reduce Your Corporation Tax Bill: Legal Strategies

1. Employer Pension Contributions

Employer pension contributions are deductible against Corporation Tax provided they pass the “wholly and exclusively for the purposes of the trade” test. A £60,000 employer pension contribution saves £15,000 in Corporation Tax at the 25% main rate, or up to £15,900 if the contribution brings profits into or out of the marginal relief band. Pension contributions also avoid employer and employee NIC, making them the most tax-efficient method of extracting value from many profitable companies.

2. Capital Allowances and Full Expensing

Companies can claim 100% tax relief on qualifying plant and machinery under Full Expensing (no monetary cap) or the Annual Investment Allowance (up to £1 million per year). Rather than depreciating assets over several years, you deduct the full cost from taxable profits in the year of purchase. For a company paying 25% Corporation Tax, spending £100,000 on qualifying equipment saves £25,000 in tax in the same accounting period.

3. Timing of Income and Expenditure

If your profits are approaching the £50,000 small profits threshold from above, bringing forward deductible expenditure (such as equipment purchases, professional fees, or subscriptions) into the current accounting period can reduce taxable profits into the 19% band. Similarly, deferring invoicing for work not yet completed may reduce profits in years when the marginal rate applies.

4. Research and Development Tax Credits

If your company undertakes qualifying R&D activity, including software development, process improvement, and technical problem-solving, not just formal scientific research, you may be able to claim an enhanced deduction against Corporation Tax or a cash credit from HMRC. The R&D merged scheme from April 2024 applies a single credit rate of 20% of qualifying expenditure for most companies.

5. Salary and Dividend Optimisation

The director’s salary is deductible against Corporation Tax. Paying a salary of £5,000 or £12,570 reduces the company’s taxable profits before Corporation Tax is calculated. The overall tax efficiency of each salary level depends on the interplay between Corporation Tax savings and the personal tax cost. This is why the calculation must be modelled for each director individually each year. Our director’s salary and dividend service includes this as standard.

ℹ️ Corporation Tax Is Paid Before Dividends Can Be Distributed

Dividends are paid from a company’s distributable profits, that is, profits after Corporation Tax has been deducted. Before declaring any dividend, you must ensure your company has sufficient distributable reserves. Our Corporation Tax service includes a year-end review of distributable reserves before any dividend planning takes place.

Want to Reduce Your Corporation Tax Bill Legally?

Our ACCA-certified accountants prepare your CT600, calculate your marginal relief correctly, and identify every allowable deduction before your accounts are filed. Fixed fee, no missed reliefs.

View Corporation Tax ServiceFrequently Asked Questions

What is the Corporation Tax rate in the UK for 2026/27?

The Corporation Tax rates for 2026/27 are 19% on profits up to £50,000 (small profits rate) and 25% on profits above £250,000 (main rate). Companies with profits between £50,000 and £250,000 benefit from marginal relief, which produces an effective rate that rises from 19% to 25% across the band. The effective marginal rate within the band is 26.5%, which is higher than the main rate, making tax planning particularly valuable for companies in this profit range.

When do I need to pay Corporation Tax?

For most small and medium-sized companies, Corporation Tax is due 9 months and 1 day after the end of the accounting period. The CT600 tax return is due within 12 months of the accounting period end. The payment deadline comes before the filing deadline. You must calculate and pay your tax bill three months before your return is due. Very large companies (taxable profits above £1.5 million) pay in quarterly instalments during the accounting period.

Does a dormant company need to pay Corporation Tax?

A dormant company is one that has had no significant accounting transactions during the accounting period and generally has no Corporation Tax liability. However, HMRC must still be notified of the company’s dormant status, and a CT600 return may still be required depending on whether the company has had any income or expenditure. You must still file a confirmation statement with Companies House each year, regardless of dormant status.

What is marginal relief for Corporation Tax?

Marginal relief reduces the Corporation Tax payable for companies with profits between £50,000 and £250,000. Rather than jumping from 19% to 25% at £50,001, the effective rate increases gradually. The marginal relief fraction used is 3/200, applied to the difference between the upper limit and the company’s profits. The practical result is an effective marginal rate of 26.5% on profits within the band. Your CT600 software calculates marginal relief automatically, and you do not need to apply the formula manually.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record