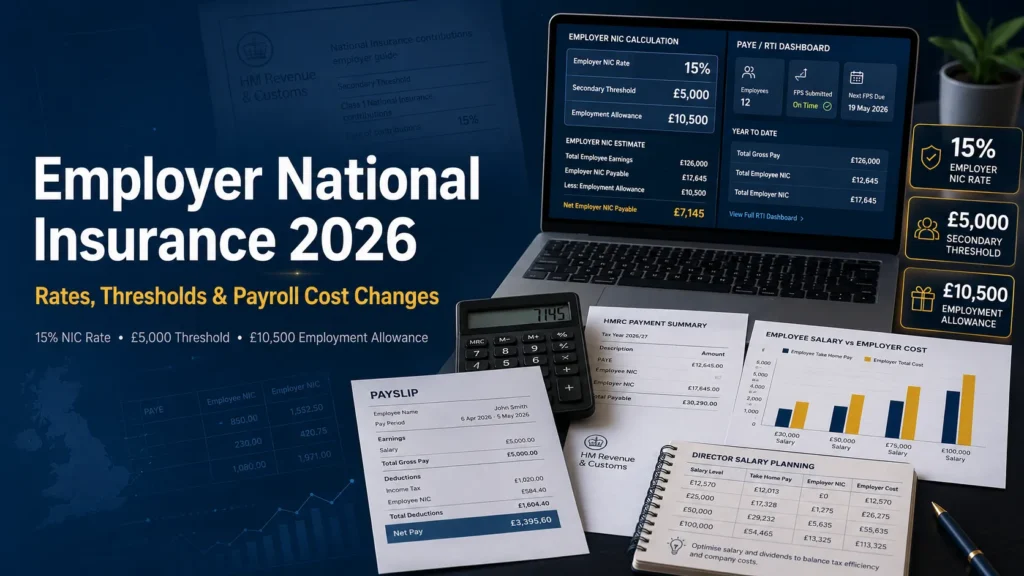

A complete 2026/27 guide for UK employers and limited company directors covering the 15% employer NIC rate, the £5,000 secondary threshold, Employment Allowance eligibility, and what these figures mean for your payroll costs and director salary strategy.

The changes to employer National Insurance that took effect from April 2025 continue to apply in 2026/27 with no further adjustment. The rate remains at 15%, and the secondary threshold remains at £5,000 per year. For many employers, a 1.2 percentage point rate rise combined with a secondary threshold cut of more than £4,000 has materially increased payroll costs compared to just two years ago. This guide explains what you owe, how to calculate it, and the planning options available to reduce your liability.

What Is Employer National Insurance?

Employer National Insurance Contributions (secondary Class 1 NICs) are a statutory cost paid by employers on top of employee wages. They are separate from the National Insurance deducted from the employee’s own pay. Employer NIC is not taken from an employee’s salary. It is an additional cost to the employer, calculated as a percentage of each employee’s earnings above the secondary threshold.

Employer NIC is reported and paid through PAYE as part of the Real Time Information (RTI) process. The monthly liability is calculated within your payroll run and included in the payment you make to HMRC by the 19th or 22nd of the following month.

Employer NIC Rates and Thresholds 2026/27

| Threshold or Rate | 2026/27 Amount | Change from Pre-April 2025 |

|---|---|---|

| Employer NIC rate (secondary Class 1) | 15% | Up from 13.8% |

| Secondary threshold (annual) | £5,000 | Down from £9,100 |

| Secondary threshold (monthly) | £417 | Down from £758 |

| Secondary threshold (weekly) | £96 | Down from £175 |

| Upper Secondary Threshold (UST) | £50,270 | Unchanged |

| Employment Allowance | £10,500 | Up from £5,000 (pre-April 2025) |

How to Calculate Employer NIC

The calculation is straightforward. For each employee, you pay 15% employer NIC on earnings above the secondary threshold of £5,000 per year. Earnings at or below £5,000 attract no employer NIC.

Example: An employee earns £30,000 per year.

- Earnings above secondary threshold: £30,000 – £5,000 = £25,000

- Employer NIC: £25,000 × 15% = £3,750 per year

Under the old threshold (£9,100):

- Earnings above old threshold: £30,000 – £9,100 = £20,900

- Employer NIC at old rate: £20,900 × 13.8% = £2,884 per year

- Additional cost per year at the same salary: £866

The Impact on Director Salary Strategy

The secondary threshold change has had a direct impact on the optimal director salary for single-director limited companies. Because the secondary threshold dropped to £5,000, a director taking a salary above £5,000 now triggers employer NIC at 15% on the excess. This is why £5,000 has become the most commonly used director’s salary. It sits at exactly the secondary threshold and eliminates employer NIC entirely, while the salary remains deductible against Corporation Tax.

| Director Salary Level | Employer NIC Cost | Income Tax on Salary | Employee NIC |

|---|---|---|---|

| £5,000 per year | £0 (at secondary threshold) | £0 (within personal allowance) | £0 (below primary threshold) |

| £12,570 per year | £1,135.50 (£7,570 × 15%) | £0 (within personal allowance) | £0 (at primary threshold) |

| £20,000 per year | £2,250 (£15,000 × 15%) | £1,486 (£7,430 × 20%) | £594 (£7,430 × 8%) |

The £12,570 salary remains worth considering for directors who can claim the Employment Allowance, because the allowance offsets the employer NIC cost. For sole directors of single-person companies who cannot claim the Employment Allowance, the £5,000 salary is generally the most NIC-efficient option. Our director salary and dividend service, payroll service, and business accounting service model the correct salary for each director’s circumstances annually.

Employment Allowance: Who Can Claim It in 2026/27?

The Employment Allowance reduces your employer NIC liability by up to £10,500 per year in 2026/27. It is claimed through an Employer Payment Summary (EPS) at the start of the tax year and applies against your monthly PAYE payments until it is used up.

You can claim the Employment Allowance if:

- You are a business or charity paying employer NIC

- You employ at least one person who is not a director, or you employ at least two directors

You cannot claim the Employment Allowance if you are a single-director company with no other employees. This restriction specifically applies to sole-director, sole-employee companies. If you have at least one employee who is not a director, such as an additional member of staff or a second director, you can claim.

⚠️ The Employment Allowance Must Be Claimed Actively — It Is Not Automatic

The Employment Allowance does not apply automatically. You must claim it each tax year by submitting an EPS with the Employment Allowance indicator set to yes. Many employers who are eligible fail to claim it and overpay NIC as a result. If you have been eligible in previous years but did not claim, you can backdate claims for up to four years. Our payroll service checks Employment Allowance eligibility at the start of every tax year.

Zero-Rate Employer NIC: Special Categories

Certain employees attract a 0% employer NIC rate up to the Upper Secondary Threshold (£50,270 per year) rather than the standard 15%. This applies to:

- Employees under 21: 0% employer NIC on earnings up to £50,270. Standard 15% applies above this threshold

- Apprentices under 25: 0% employer NIC on earnings up to £50,270, provided they are in a government-approved apprenticeship scheme

- Armed forces veterans in their first year of civilian employment: 0% employer NIC on earnings up to £50,270

Class 1A and Class 1B NIC: Benefits and PAYE Settlement Agreements

In addition to standard Class 1 employer NIC on salaries, employers may also owe:

- Class 1A NIC at 15%: Payable on the value of taxable benefits in kind reported on P11D forms. Due by 22 July, following the end of the tax year

- Class 1B NIC at 15%: Payable on benefits covered by a PAYE Settlement Agreement (PSA). Due by 22 October, following the end of the tax year

Is Your Payroll Calculating Employer NIC Correctly?

Our payroll outsourcing service ensures every NIC calculation is correct, Employment Allowance is claimed where eligible, and director salaries are set at the right level each year. Fixed fee, filed on time.

View Payroll ServiceFrequently Asked Questions

What is the employer NIC rate for 2026/27?

The employer NIC rate for 2026/27 is 15% on earnings above the secondary threshold of £5,000 per year. This rate was increased from 13.8%, and the secondary threshold was reduced from £9,100, both changes taking effect from 6 April 2025. Both remain unchanged for 2026/27.

What is the employer NIC secondary threshold for 2026/27?

The employer NIC secondary threshold is £5,000 per year (£417 per month, £96 per week) for 2026/27. Employer NIC is charged at 15% on earnings above this threshold. The reduction from the previous £9,100 threshold means employers now pay NIC on a larger portion of lower-wage employees’ earnings than before April 2025.

Can a single-director company claim the Employment Allowance?

No. A company where the sole director is also the only employee cannot claim the Employment Allowance. If you employ at least one other person who is not a director, or you have two or more directors on the payroll, the company can claim. The allowance reduces your employer’s NIC liability by up to £10,500 in 2026/27 and must be actively claimed through an EPS each tax year.

Why is the optimal director salary £5,000 in 2026/27?

For sole directors of single-person companies who cannot claim the Employment Allowance, a salary of £5,000 per year sits exactly at the employer NIC secondary threshold. This means no employer NIC is payable on the salary. The salary falls below the employee NIC primary threshold (£12,570) and within the personal allowance, so no employee NIC or Income Tax is payable either. The salary is deductible against Corporation Tax at 19% or 25%, reducing the company’s taxable profits. This makes £5,000 the most NIC-efficient salary for most sole directors in 2026/27, though your exact optimal salary depends on your Employment Allowance eligibility and other circumstances.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record