Stamp Duty Land Tax is the largest upfront cost in most property transactions. A landlord purchasing a £350,000 buy-to-let property in London in 2026 pays £23,250 in SDLT before spending a penny on the property itself — £15,750 more than a standard buyer pays on the same property. Understanding the current rate structure, surcharges, and the legitimate planning options available in 2026 is essential before committing to any transaction. This guide from the landlord tax specialists at Protax Consultants covers the full SDLT picture for England and Northern Ireland.

What Is Stamp Duty Land Tax?

Stamp Duty Land Tax is the tax charged on property purchases in England and Northern Ireland. Scotland uses Land and Buildings Transaction Tax and Wales uses Land Transaction Tax, each with separate rate structures. This guide covers SDLT only.

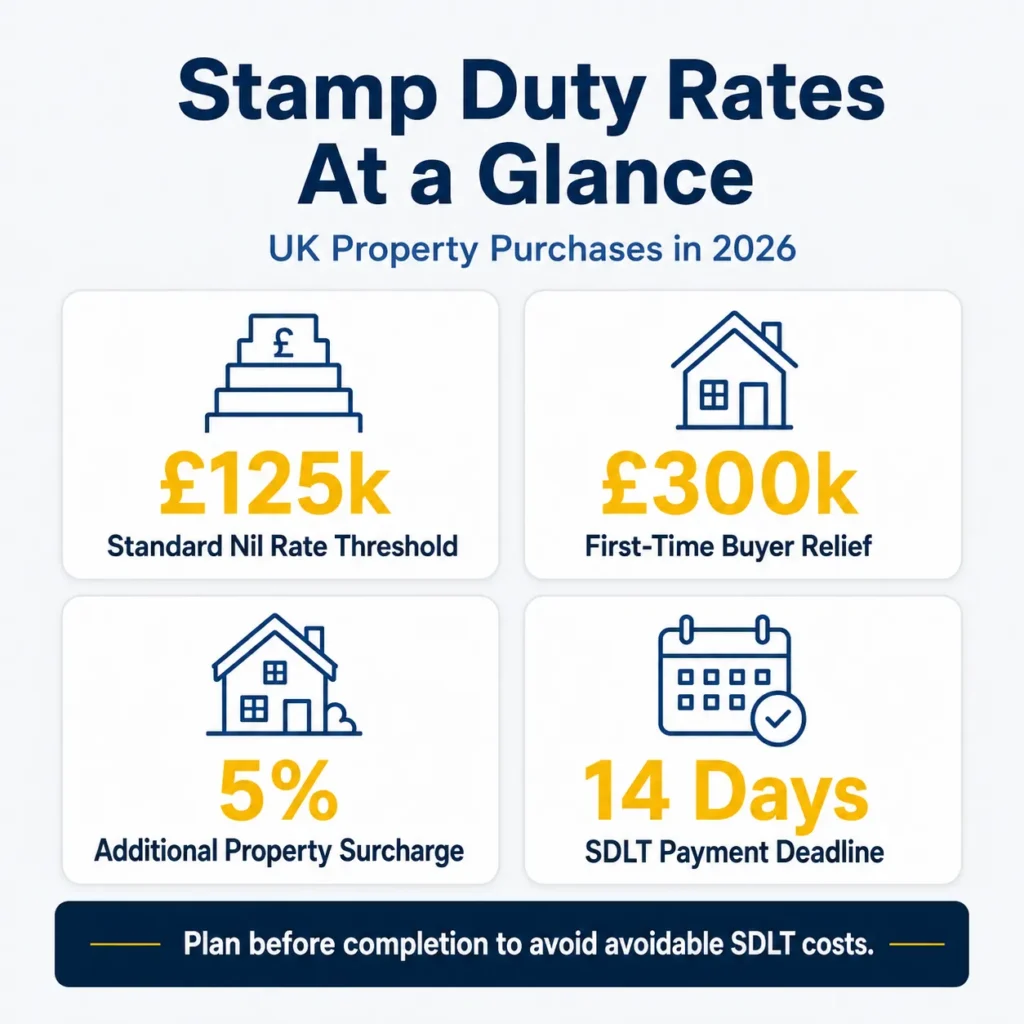

SDLT is calculated on a tiered basis — each slice of the purchase price falls into a separate rate band. The rate for one band does not apply to the entire purchase price. SDLT must be reported and paid within 14 days of the completion date. Your conveyancer handles the return and payment from completion funds and issues you an SDLT5 certificate, which the Land Registry requires to register the title.

Standard Residential SDLT Rates 2026

The current residential SDLT rate structure has been in place since 1 April 2025, when the temporary Covid-era thresholds were removed. Rates apply to the portion of the purchase price within each band only.

| Purchase Price Band | Standard Rate | Effective on Band |

| Up to £125,000 | 0% | £0 |

| £125,001 to £250,000 | 2% | £2,500 max |

| £250,001 to £925,000 | 5% | £33,750 max |

| £925,001 to £1,500,000 | 10% | £57,500 max |

| Above £1,500,000 | 12% | No cap |

Worked Example: Standard Buyer at £400,000

| Band | Taxable Amount | Rate | Tax |

| £0 to £125,000 | £125,000 | 0% | £0 |

| £125,001 to £250,000 | £125,000 | 2% | £2,500 |

| £250,001 to £400,000 | £150,000 | 5% | £7,500 |

| Total SDLT | £400,000 | Eff. 2.5% | £10,000 |

First-Time Buyer Relief 2026

First-time buyers purchasing a residential property in England and Northern Ireland pay no SDLT on the first £300,000 of the purchase price. On the portion between £300,001 and £500,000, a 5% rate applies. No relief is available on properties above £500,000.

All buyers in the transaction must qualify as first-time buyers. A first-time buyer is someone who has never owned a residential property anywhere in the world.

| Purchase Price | First-Time Buyer SDLT | Standard Buyer SDLT |

| £250,000 | £0 | £2,500 |

| £350,000 | £2,500 | £7,500 |

| £450,000 | £7,500 | £10,000 |

| £500,000 | £10,000 | £12,500 |

| £600,000 | No relief — £22,500 | £22,500 |

The Additional Property Surcharge for Landlords

Anyone who already owns one or more residential properties anywhere in the world and purchases an additional residential property above £40,000 pays SDLT at an additional rate. The surcharge is 5% on every SDLT band, added on top of the standard rates. This surcharge increased from 3% to 5% on 31 October 2024 and the higher rate remains in force for 2026. For the ongoing income tax implications once you own the property, see our complete buy-to-let tax guide for 2026.

| Purchase Price Band | Standard Rate | + 5% Surcharge | Combined Rate |

| Up to £125,000 | 0% | +5% | 5% |

| £125,001 to £250,000 | 2% | +5% | 7% |

| £250,001 to £925,000 | 5% | +5% | 10% |

| £925,001 to £1,500,000 | 10% | +5% | 15% |

| Above £1,500,000 | 12% | +5% | 17% |

Worked Example: Buy-to-Let at £350,000

| Band | Taxable Amount | Combined Rate | Tax |

| £0 to £125,000 | £125,000 | 5% | £6,250 |

| £125,001 to £250,000 | £125,000 | 7% | £8,750 |

| £250,001 to £350,000 | £100,000 | 10% | £10,000 |

| Total SDLT (landlord) | £350,000 | Eff. 6.6% | £25,000 |

| Standard buyer SDLT on same property | £350,000 | Eff. 2.1% | £7,500 |

| Surcharge premium paid by landlord | £17,500 |

Worked Example: Buy-to-Let at £600,000

| Band | Taxable Amount | Combined Rate | Tax |

| £0 to £125,000 | £125,000 | 5% | £6,250 |

| £125,001 to £250,000 | £125,000 | 7% | £8,750 |

| £250,001 to £600,000 | £350,000 | 10% | £35,000 |

| Total SDLT (landlord) | £600,000 | Eff. 8.3% | £50,000 |

| Standard buyer SDLT on same property | £600,000 | Eff. 3.7% | £22,500 |

| Surcharge premium paid by landlord | £27,500 |

Company Purchases

Companies buying residential property below £500,000 pay the same additional dwelling surcharge as individuals. Above £500,000, companies face a flat rate of 15% unless specific property rental business reliefs apply. Most buy-to-let companies use the banded rates with the 5% surcharge on properties under £500,000, as the flat 15% corporate rate is materially more expensive. For the ongoing tax treatment of company-owned property, see our Corporation Tax service.

| Buyer Type | SDLT on £350k | SDLT on £600k | Key Rate |

| Standard home mover | £7,500 | £22,500 | 0–12% bands |

| First-time buyer | £2,500 | £22,500* | 0% up to £300k |

| Buy-to-let / second home | £25,000 | £50,000 | +5% surcharge |

| Non-resident buy-to-let | £30,500 | £62,000 | +5% +2% surcharges |

| Company (under £500k) | £25,000 | N/A | +5% surcharge |

| Company (over £500k) | N/A | £90,000 | 15% flat rate |

* FTB relief does not apply above £500,000 — standard rates apply in full.

The Non-Resident Surcharge

Buyers who have not been present in the UK for at least 183 days in the 12 months before the completion date pay an additional 2% surcharge on top of all other applicable SDLT rates. A non-resident buying a buy-to-let property pays the standard rates, the 5% additional property surcharge, and the 2% non-resident surcharge, making a combined additional rate of 7% on every band.

The non-resident surcharge can be refunded if the buyer becomes a UK resident within two years of the transaction, having spent at least 183 days in the UK in the 12 months immediately after completion.

| Non-Resident Buy-to-Let: How the Combined Surcharges Stack |

| Standard rate (e.g. 5% on £250k–£925k band) + 5% additional property surcharge + 2% non-resident surcharge = 12% combined on that band. On a £350,000 buy-to-let purchase by a non-resident, the effective rate rises to approximately 8.7%, versus 6.6% for a UK-resident landlord. |

The 36-Month Surcharge Refund

If a buyer paid the 5% additional property surcharge at the time of purchase because they owned another property, and they subsequently sell that previous property within 36 months of the new purchase, they can apply to HMRC for a refund of the surcharge. The application must be made within 12 months of the disposal.

This refund entitlement applies primarily to buyers replacing their main residence during a gap between selling and buying. Contact your conveyancer or our tax team to make the claim within the permitted window.

| Step | Action | Deadline |

| 1 | Pay 5% surcharge at purchase | At completion (14-day deadline) |

| 2 | Sell previous property | Must complete within 36 months of new purchase |

| 3 | Apply to HMRC for refund | Within 12 months of disposal of previous property |

What Happened to Multiple Dwellings Relief?

| Multiple Dwellings Relief was abolished — 1 June 2024 |

| MDR, which allowed buyers purchasing two or more residential properties in a single transaction to calculate SDLT based on the average price per dwelling, was abolished from 1 June 2024. It is no longer available for any transaction in 2026. Buyers purchasing multiple residential properties in a single transaction now pay SDLT on the full combined price without any averaging. |

Legitimate Ways to Reduce Your SDLT Bill in 2026

| Strategy | How It Works | Risk Level |

| Mixed-use classification | Non-residential SDLT rates apply — no surcharge, lower bands (0% to £150k, 2% to £250k, 5% above) | Medium — HMRC scrutinises this area closely |

| Surcharge refund | Claim back 5% surcharge if previous property sold within 36 months | Low — straightforward if conditions met |

| Completion date coordination | Avoid owning two properties simultaneously — surcharge never applies | Low — depends on transaction alignment |

| Price negotiation at thresholds | Keeping price below £925k avoids the 10% band; meaningful saving when surcharges are included | Low — commercial negotiation |

| Non-resident refund | Claim back 2% surcharge if you become UK resident within 2 years | Low — apply within the refund window |

Mixed-Use Property Classification

Commercial or mixed-use properties attract lower SDLT rates with no additional property surcharge. The non-residential rate structure is 0% up to £150,000, 2% on £150,001 to £250,000, and 5% above £250,000. A property with a genuine mixed-use classification, such as a shop with a residential flat above, may qualify for these lower rates. The classification must be genuine and properly evidenced. HMRC challenges mixed-use claims regularly, and applying non-residential rates to a clearly residential property carries significant enquiry and penalty risk.

Claiming the Surcharge Refund

Where the 5% surcharge was paid and the previous property is sold within 36 months, filing the refund claim within 12 months of the disposal is a straightforward saving that is easy to overlook without a reminder system in place.

Completion Date Coordination

For buyers simultaneously selling a main residence and purchasing a new one, coordinating completion dates to avoid owning both properties simultaneously can prevent the surcharge applying entirely. This eliminates the surcharge rather than recovering it after the event.

Price Negotiation at Threshold Points

At £925,000, the SDLT rate increases from 5% to 10% on the next slice. With the additional property surcharge, crossing that threshold costs materially more than the price difference. A modest negotiation from £930,000 to £925,000 saves significantly more than £5,000 once surcharges are included.

How SDLT Interacts with Other Property Taxes

SDLT is one part of the overall property tax picture for landlords. Once the property is owned, Section 24 restricts mortgage interest relief to a 20% tax credit, significantly increasing income tax for higher-rate landlords. On eventual disposal, Capital Gains Tax applies at 18% or 24% on the gain, with a 60-day reporting deadline. Our complete buy-to-let tax guide for 2026 covers the full tax lifecycle from acquisition to disposal.

| Stage | Tax | Rate / Treatment | Key Deadline |

| Purchase | SDLT | Standard + 5% surcharge | 14 days from completion |

| Annual rental | Income Tax (Section 24) | 20% / 40% / 45% — 20% mortgage interest credit only | 31 Jan Self Assessment |

| Annual rental | MTD (from Apr 2026) | Quarterly digital reporting if income over £50,000 | 7 Aug / 7 Nov / 7 Feb / 7 May |

| Disposal | Capital Gains Tax | 18% (basic) / 24% (higher rate) | 60 days from completion |

Frequently Asked Questions

What is the Stamp Duty rate for a buy-to-let property in 2026?

Landlords and second-home buyers pay SDLT at standard residential rates plus a 5% surcharge on every band. The combined rates are 5% on the first £125,000, 7% on £125,001 to £250,000, 10% on £250,001 to £925,000, 15% on £925,001 to £1,500,000, and 17% above £1,500,000. The surcharge increased from 3% to 5% on 31 October 2024 and applies to all purchases of additional residential properties above £40,000.

When did SDLT rates change for 2026?

The current rate structure has been in place since 1 April 2025. The standard nil-rate threshold returned to £125,000. First-time buyer relief reduced from £425,000 to £300,000. The additional property surcharge had already increased from 3% to 5% on 31 October 2024. There were no further SDLT rate changes in April 2026.

How long do I have to pay Stamp Duty after completion?

SDLT must be reported and paid within 14 days of the completion date. Your conveyancer handles this as part of the completion process, deducting the SDLT from the funds provided at completion and filing the SDLT1 return with HMRC.

Can I get a refund of the additional property surcharge?

Yes. If you paid the 5% surcharge because you owned another property at the time of purchase, and you sell that property within 36 months of the new purchase, you can claim a refund. The application must be made within 12 months of the disposal. Contact our tax team to handle the claim within the permitted window.

Does Multiple Dwellings Relief still exist in 2026?

No. Multiple Dwellings Relief was abolished for residential property purchases completing on or after 1 June 2024. Buyers purchasing multiple residential properties in a single transaction now pay SDLT on the full combined price without the averaging calculation MDR previously allowed.

Where can I get SDLT and property tax advice in London?

Protax Consultants are ACCA-qualified accountants based in Wimbledon, London. Our landlord property tax service covers SDLT planning, Section 24 management, and Capital Gains Tax advice for property transactions across London and Surrey. Visit our landlords sector page or call 020 8545 7451.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record