A practical 2026/27 guide for UK freelancers, sole traders, and new founders comparing the tax, liability, admin, and profit thresholds of each business structure — with real numbers.

It is one of the most searched questions in UK business: should I be a sole trader or set up a limited company? The answer depends on how much you earn, how much risk you carry, and how much admin you are willing to take on. This guide covers every key difference so you can make an informed decision — or speak to one of our ACCA-certified accountants who can model it precisely for your situation.

What Is a Sole Trader?

A sole trader is a self-employed individual who runs their own business personally. There is no legal separation between you and your business. You keep all profits after tax, but you are personally liable for all debts and obligations.

Setting up is simple: register with HMRC as self-employed, file a Self Assessment tax return each year, and pay Income Tax and National Insurance Contributions (NICs) on your profits.

What Is a Limited Company?

A limited company is a separate legal entity registered at Companies House. The company owns its own assets, enters contracts in its own name, and pays Corporation Tax on its profits. As a director and shareholder, you are separate from the business — your personal liability is limited to what you have invested.

Most directors of small limited companies pay themselves a combination of a low salary and dividends. This is the core of the tax efficiency argument for incorporating — but it is not always the right answer for everyone.

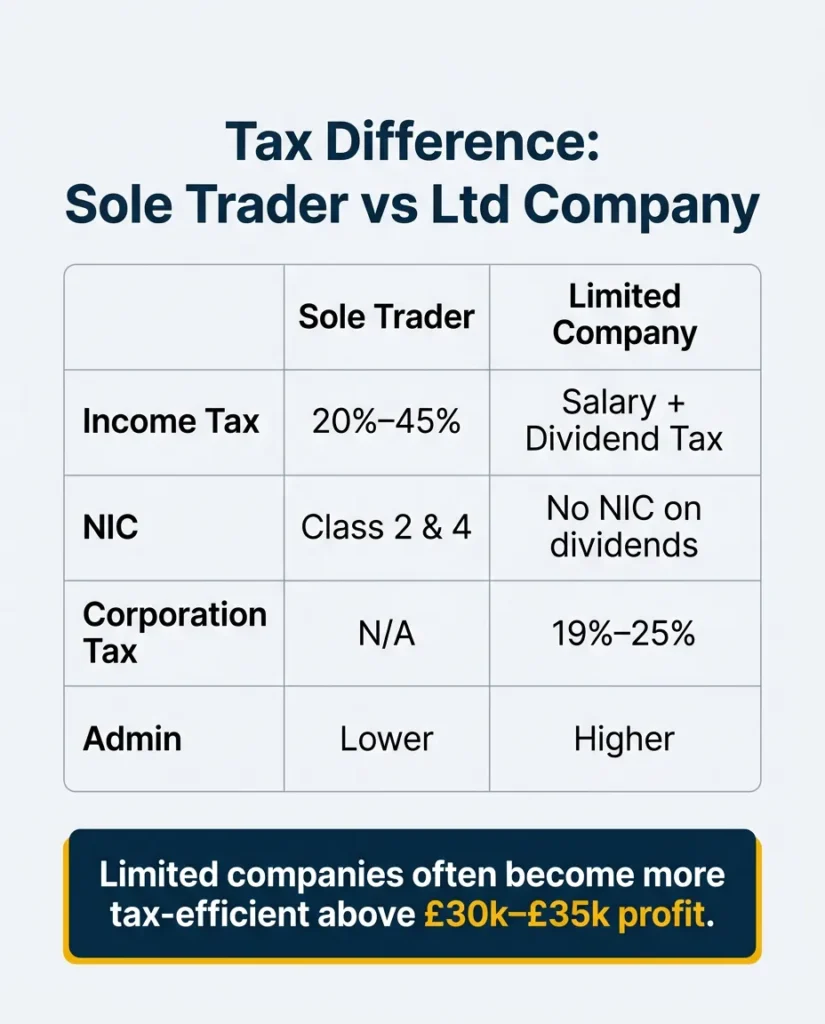

Sole Trader vs Limited Company: The Key Differences at a Glance

| Factor | Sole Trader | Limited Company |

|---|---|---|

| Legal identity | You are the business | Separate legal entity |

| Personal liability | Unlimited — you are personally liable | Limited to your investment |

| Tax on profits | Income Tax (20%–45%) + NICs | Corporation Tax (19%–25%) |

| How you pay yourself | Drawings from profits | Salary + dividends |

| Admin burden | Lower — Self Assessment only | Higher — annual accounts, confirmation statement, payroll |

| Privacy | Accounts not public | Accounts filed at Companies House (publicly visible) |

| Business credibility | Can be perceived as smaller | Often seen as more established |

| Pension contributions | Personal contributions only | Company can contribute (tax efficient) |

The Tax Difference: Sole Trader vs Limited Company in 2026/27

This is the most important section for most people. The tax comparison depends heavily on your profit level. Here is how it works.

How Sole Traders Are Taxed

As a sole trader, you pay Income Tax on your net profits after allowable expenses. The rates for England, Wales and Northern Ireland in 2026/27 are:

- 0% on the first £12,570 (personal allowance)

- 20% on profits from £12,571 to £50,270 (basic rate)

- 40% on profits from £50,271 to £125,140 (higher rate)

- 45% on profits above £125,140 (additional rate)

On top of Income Tax, sole traders also pay National Insurance Contributions. For 2026/27, Class 4 NICs are charged at 6% on profits between £12,570 and £50,270, and 2% above £50,270. Mandatory Class 2 NICs no longer apply in the same way for most self-employed people, although voluntary Class 2 contributions may still be relevant if profits are below the Small Profits Threshold and you want to protect your National Insurance record.

ℹ️ The Numbers Are Closer Than People Think at £60k

At £60,000 profit, the after-tax difference between sole trader and limited company is relatively small once you account for Corporation Tax. The tax savings become much more significant at higher profit levels, or when pension planning and spouse shareholding are factored in.

How Limited Company Directors Are Taxed

A limited company pays Corporation Tax on its profits — 19% on profits up to £50,000, and 25% on profits above £250,000. Rates taper between these thresholds through Marginal Relief.

As a director, you typically pay yourself a small salary and take the rest as dividends. For 2026/27, dividends above the dividend allowance are taxed at 10.75% in the basic rate band, 35.75% in the higher rate band, and 39.35% in the additional rate band. Dividends are not subject to National Insurance, but they are paid from company profits after Corporation Tax. Our business accounting service includes annual salary and dividend planning as standard for every director client.

Side-by-Side Tax Comparison: £60,000 Profit in 2026/27

| Sole Trader | Limited Company Director | |

|---|---|---|

| Dividends taken from the remaining profit | £60,000 | £60,000 |

| Corporation Tax (Ltd only) | — | approx. £9,000 |

| Salary taken | — | £12,570 |

| Income Tax/dividend tax payable (personal) | — | approx. £38,400 |

| Income Tax / dividend tax payable (personal) | approx. £11,400 | approx. £4,100 |

| National Insurance (personal) | approx. £2,500 | £0 on dividends |

| Total tax & NIC | approx. £13,900 | approx. £13,100 |

| Take-home pay | approx. £46,100 | approx. £46,900 |

⚠️ Warning: This £60k Example Is Only an Illustration

The limited company example assumes a simple salary and dividend extraction model and does not include every possible adjustment, such as employer National Insurance on salary, Employment Allowance eligibility, pension contributions, associated company rules, personal circumstances, student loan repayments, Scottish tax rates, or other income. The correct answer can change significantly once your exact numbers are modelled.

When Does a Limited Company Make Financial Sense?

Incorporating is generally worth considering when:

- Your net profit is consistently above £30,000–£35,000 per year and is growing

- You do not need to draw all your profits immediately — retained profits in a company are taxed at Corporation Tax rates, not the higher personal Income Tax rates

- You want to split income with a spouse or civil partner, provided both hold genuine shares and the arrangement is commercially sensible

- You want the company to make employer pension contributions on your behalf

- You work in a sector where clients or contracts require you to operate through a company, which is common in IT, construction, consultancy and professional services

- You want to limit your personal financial liability

When Staying a Sole Trader Makes More Sense

There is no shame in staying a sole trader. It is simpler, cheaper to run, and often the right structure for the early stages of a business. A sole trader is usually the better choice when:

- Your annual profit is consistently below £25,000

- You are just starting out, and your income is uncertain

- You want to keep admin and accountancy costs low

- You plan to wind down the business or retire within a few years

- Your clients do not require a company structure

The Hidden Costs of Running a Limited Company

Running a limited company involves more administration than being a sole trader. Before you incorporate, it is worth understanding the ongoing obligations:

- Annual accounts: Must be filed at Companies House every year, prepared to accounting standards

- Corporation Tax return (CT600): Filed with HMRC after each accounting year

- Confirmation statement: An annual filing confirming your company details at Companies House

- Payroll (PAYE): Even a small director’s salary may require a PAYE scheme and regular Real Time Information (RTI) submissions to HMRC

- Self Assessment: Directors may still need to file a personal Self Assessment tax return for their salary, dividends and other personal income

- Dividend administration: Every dividend payment must be backed by board minutes and a dividend voucher. Dividends paid without sufficient distributable profits are unlawful under the Companies Act 2006

These are all manageable with the right accountant, but they are real ongoing responsibilities. Our small business accounting service handles all of the above for limited company clients at a fixed monthly fee.

What About VAT? Does Your Structure Affect VAT Registration?

VAT registration is separate from your business structure. Whether you are a sole trader or a limited company, you must register for VAT once your taxable turnover exceeds £90,000 in any rolling 12-month period. The structure you choose does not change your VAT obligations, but it does affect how VAT is administered — a limited company files VAT returns in the company’s name, while a sole trader files in their own name.

Sole Trader vs Limited Company: The IR35 Consideration

If you work through a limited company providing services to larger organisations — particularly in IT, finance, engineering, consultancy or public sector roles — IR35 is a critical consideration. IR35 is anti-avoidance legislation designed to ensure that contractors who work like employees pay broadly the same tax as employees, even if they operate through a limited company.

Being caught by IR35 significantly reduces the tax advantage of a limited company structure for that income. If IR35 is a risk in your sector, it is important to get a proper working practice review before deciding to incorporate. The HMRC Check Employment Status for Tax (CEST) tool provides an initial assessment, but it is not always conclusive.

Switching from Sole Trader to Limited Company: What Is Involved?

Incorporating an existing sole trader business is a straightforward process. The key steps are:

- Incorporate the limited company at Companies House

- Open a separate business bank account in the company’s name

- Transfer any business assets into the company — this may have tax implications depending on the asset values

- Notify HMRC of the change in your trading status

- Set up PAYE for the director’s salary where required

- Continue filing your final sole trader Self Assessment return for the period before incorporation

If you are considering switching, it is worth taking advice on the timing — particularly if your business holds significant assets or has ongoing contracts. Our team at Protax Consultants works with new founders and growing businesses across London and the UK to get the structure right from the beginning.

Quick Decision Guide: Sole Trader or Limited Company?

| Your Situation | Likely Best Structure |

|---|---|

| Annual profit below £25,000 and just starting out | Sole trader |

| Annual profit £30,000–£50,000 and growing | Worth modelling both — book a consultation |

| Annual profit above £50,000 consistently | Limited company may be more tax-efficient, depending on drawings and retained profits |

| Working in IT or professional services for large clients | Limited company may help commercially, but check IR35 position |

| Want to involve spouse as shareholder | Limited company, with correct share structure and proper advice |

| Want to retain profits in the business | Limited company |

| Minimal admin preference, low income level | Sole trader |

Not Sure Which Structure Is Right for You?

Our ACCA-certified accountants model the exact tax difference for your profit level and circumstances — including salary, dividends, NICs, Corporation Tax, pension contributions and retained profits. Fixed fee, no jargon, clear recommendation.

Get a Free QuoteFrequently Asked Questions

What is the main difference between a sole trader and a limited company?

The main difference is legal identity and liability. A sole trader and their business are one and the same — you are personally liable for all debts. A limited company is a separate legal entity; your personal liability is limited to what you have invested. From a tax perspective, sole traders pay Income Tax and National Insurance on all profits, while a limited company pays Corporation Tax on profits, and the director pays tax on salary and dividends separately.

At what income level is a limited company more tax-efficient?

This depends on your individual circumstances, but as a general rule, the tax savings from a limited company structure start to become meaningful once your annual profit exceeds £30,000–£35,000 and you do not need to draw every pound immediately. The savings are usually more significant where profits are retained in the company, pension contributions are planned properly, or shareholders are structured correctly. Below that level, the additional accountancy costs and administration of running a company may outweigh any tax savings.

Can I be a sole trader and have a limited company at the same time?

Yes. Some people operate a limited company for their main trading activity while retaining sole trader status for a separate, lower-income activity. Both tax positions must be reported correctly — the company files its own accounts and Corporation Tax return, while the individual files a Self Assessment return covering sole trader income, director’s salary, dividends, and any other personal income.

Do sole traders pay less tax than limited companies?

Not necessarily. At lower profit levels, the overall tax burden can be similar or even lower as a sole trader once you account for Corporation Tax, dividend tax, payroll requirements and the cost of running a company. At higher profit levels, a well-structured limited company can be more tax-efficient, particularly if profits are retained in the company or used for pension contributions. However, the answer depends on your specific circumstances — there is no universal rule.

How do I register as a sole trader in the UK?

You register as a sole trader by registering for Self Assessment with HMRC. You must do this by 5 October, following the end of the tax year in which you first became self-employed. Once registered, you file a Self Assessment tax return each year, reporting your business income and expenses and paying Income Tax and National Insurance on your net profits.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record