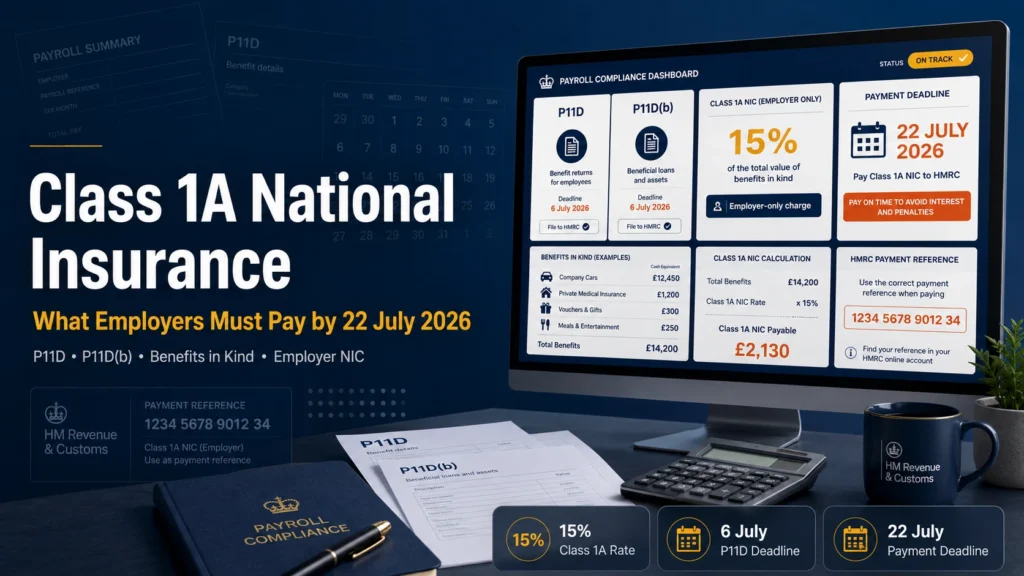

If your company provided employees or directors with benefits in kind during the 2025/26 tax year, two deadlines are now approaching fast. The P11D and P11D(b) forms must reach HMRC by 6 July 2026. The Class 1A National Insurance bill that sits behind those forms must be paid by 22 July 2026 if you are paying electronically, or by 19 July 2026 if paying by post.

Miss either date and HMRC begins charging penalties automatically, with no grace period and no discretionary warning. This guide from the payroll specialists at Protax Consultants explains exactly what Class 1A NIC is, how to calculate it, what happens if you are late, and why this July carries extra significance as the P11D system approaches its final year.

What Is Class 1A National Insurance?

Class 1A National Insurance is an employer-only charge on the taxable value of benefits in kind provided to employees and directors. Unlike Class 1 NIC, which is shared between employer and employee and deducted through payroll, Class 1A is paid entirely by the company and does not reduce the employee’s take-home pay.

The charge applies to the total value of benefits reported on your P11D forms. Common examples include company cars and fuel, private medical insurance, beneficial loans, living accommodation, gym memberships and non-cash vouchers. The rate for 2025/26 is 15% of the taxable benefit value, in line with the secondary employer NIC rate that increased in April 2025.

Two forms are involved. The P11D reports the individual benefits provided to each employee or director. The P11D(b) is the employer-level summary that declares the total Class 1A NIC liability on everything reported. You must file both, even if you have already been payrolling some benefits voluntarily. For a full picture of employer costs beyond benefits, see our guide to the true cost of employing someone in 2026.

The Key Deadlines for July 2026

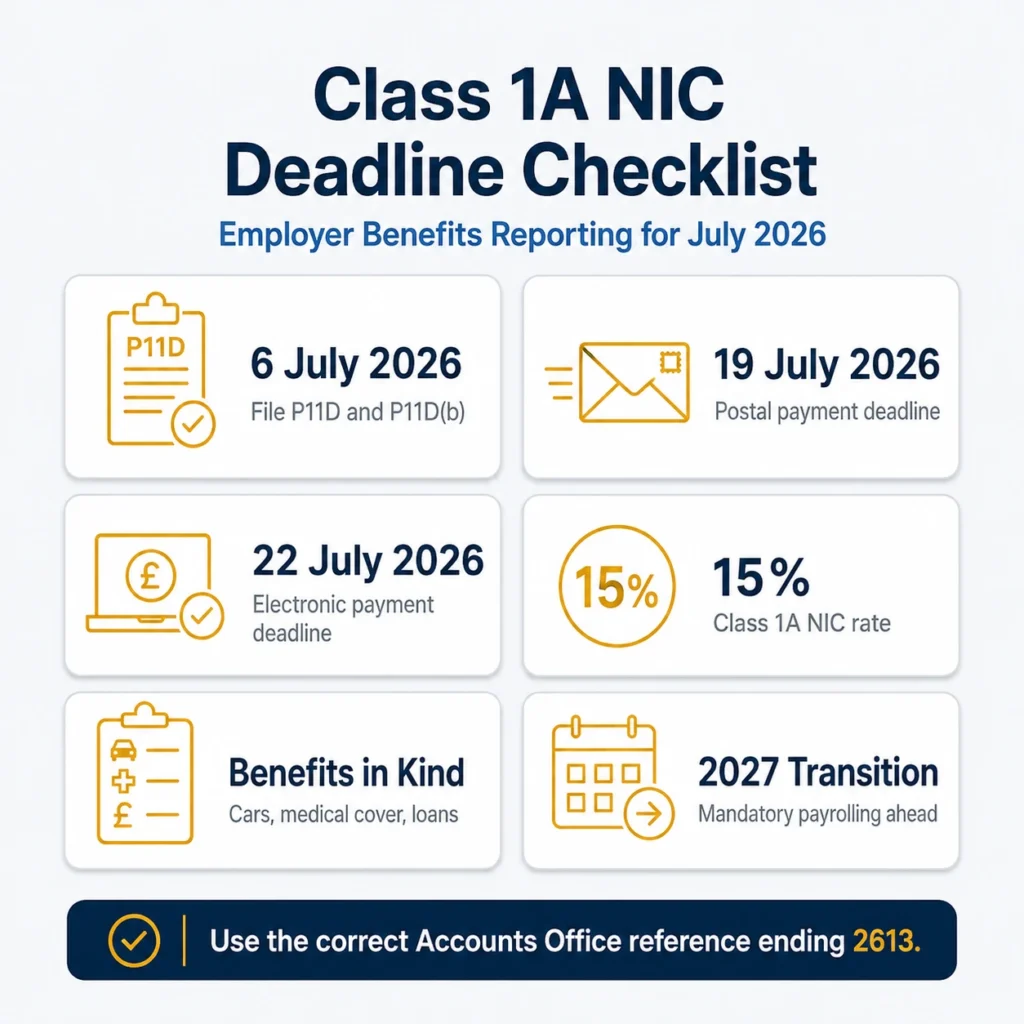

Three dates matter for the 2025/26 tax year.

6 July 2026 is the deadline to submit all P11D and P11D(b) forms to HMRC electronically, and to provide each employee with a copy of their P11D information.

19 July 2026 is the payment deadline for Class 1A NIC if you are paying by cheque or post.

22 July 2026 is the payment deadline if you are paying electronically. This is the date the cleared funds must be in HMRC’s account, not the date you initiate the transfer.

The payment reference for Class 1A NIC is your 13-character Accounts Office reference followed by the digits 2613. The 26 identifies the tax year ended 5 April 2026, and the 13 identifies the payment as Class 1A. Using the wrong reference is one of the most common reasons payments are misallocated, and chase letters are issued.

Important: HMRC no longer accepts paper P11D forms. Everything must be submitted electronically, either through HMRC’s PAYE Online service or through compatible payroll software. If your previous process involved posting forms, you need to change your method before 6 July.

How to Calculate Your Class 1A NIC Liability

The calculation is straightforward. Add up the taxable value of every benefit reported across all P11D forms. Multiply the total by 15%. The result is the Class 1A NIC you owe for 2025/26.

The practical challenge is identifying and valuing every benefit correctly. Each category of benefit has its own HMRC valuation method, and errors in valuation carry their own inaccuracy penalties, separate from any late-filing charge.

- Company cars: the taxable benefit depends on the car’s list price and its CO2 emissions figure, for which HMRC updates the appropriate percentage each year.

- Private medical insurance: the taxable value is the cost to the employer, not the market value of the cover, and group policy premiums must be correctly allocated per employee.

- Beneficial loans: since April 2025, HMRC reviews the official rate of interest on loans quarterly rather than annually, so the rate used in the calculation must reflect the correct quarterly figure.

- Payrolled benefits: where you have voluntarily payrolled benefits, income tax has already been collected through the payslip, but Class 1A NIC may still be due and must be declared on a P11D(b) unless HMRC has confirmed otherwise.

Common Reportable Benefits and Their Treatment

| Benefit | Taxable value basis | Class 1A NIC applies? |

|---|---|---|

| Company car | List price x CO2 appropriate percentage | Yes |

| Car fuel benefit | Fixed multiplier x CO2 percentage | Yes |

| Private medical insurance | Cost to employer | Yes |

| Beneficial loan | Interest below HMRC official rate x loan balance | Yes — excluded from mandatory payrolling post-2027 |

| Living accommodation | Annual value or cost, depending on circumstances | Yes — excluded from mandatory payrolling post-2027 |

| Gym membership | Cost to employer | Yes |

| Trivial benefits (under £50, not cash) | Not reportable | No |

| Business mileage at HMRC approved rate | Not reportable if within AMAP rates | No |

| Workplace nursery provision | Exempt | No |

Two benefit categories are excluded from mandatory payrolling even after April 2027 and will remain on P11D reporting: beneficial loans and living accommodation. If you assume the P11D obligation ends entirely after 2026/27, you will remain non-compliant.

What Happens If You Miss the Deadlines?

HMRC charges penalties automatically from the moment a deadline passes. There is no warning letter before the penalty starts.

For a late P11D(b), the penalty is £100 per 50 employees for each month or part month the return is outstanding. HMRC issues penalty notices quarterly until the form is received, so a three-month delay could generate multiple notices before you have spotted the issue.

For a late Class 1A NIC payment, HMRC charges interest on the outstanding balance from 22 July. Additional percentage penalties apply after 30 days (5%), six months (a further 5%) and twelve months (a further 5%). For a business with ten employees each receiving a company car, a six-month delay can easily generate penalties exceeding the original NIC bill.

An inaccurate P11D carries a separate inaccuracy penalty of up to £3,000 per incorrect form, depending on whether the error is considered careless or deliberate.

If you receive a P11D(b) reminder from HMRC but have no Class 1A NIC to declare, you must still respond to confirm no return is due. Ignoring the notice allows the system to assume a return is expected, and penalties will follow as if you had filed late.

The P11D Transition: Why This Year Matters More Than Usual

From 6 April 2027, mandatory payrolling of benefits in kind replaces the P11D process for most employers. Benefits will be reported and taxed in real time through payroll rather than declared once a year after the tax year ends. For many businesses, July 2026 is therefore one of the last times they will go through the traditional P11D process.

This creates two specific risks to plan for now. First, July 2027 will be unusually expensive. Employers will owe the full Class 1A NIC lump sum for 2026/27 in the traditional way, and simultaneously begin making real-time monthly Class 1A payments on payrolled benefits. Finance teams that do not set funds aside in advance will face a cash flow squeeze.

Second, employees need to be briefed before April 2027. When benefits move into payroll, the tax on them is deducted from each monthly pay packet. Employees who receive company cars, private medical cover or other benefits will see a reduction in their net pay from April 2027 onwards, even though the gross value of their package has not changed.

The window to register for voluntary payrolling of benefits for the 2026/27 tax year has already closed. Employers wanting to adopt it now will need to wait until the registration window opens for 2027/28, which HMRC expects to make available in November 2026.

What Directors Need to Know Specifically

Company directors are treated as employees for benefits-in-kind purposes. If your limited company provides you with a company car, private medical insurance, a director’s loan at a rate below HMRC’s official rate, or any other benefit, those items must be reported on your P11D and the Class 1A NIC included in the P11D(b) calculation.

One common confusion for director-shareholders is the distinction between benefits in kind and dividends. Dividends do not attract Class 1A NIC, but benefits provided through the company do, regardless of whether the director is also a shareholder. For a director’s year-end payroll overview, see our guide to understanding the P60.

Your July 2026 Class 1A Checklist

- Identify every employee and director who received a taxable benefit in 2025/26 that was not payrolled.

- Calculate the taxable value of each benefit using HMRC’s correct valuation method for that category.

- Prepare the individual P11D forms and the P11D(b) summary declaration.

- Submit everything electronically to HMRC and send each employee their P11D information by 6 July 2026.

- Calculate your Class 1A NIC at 15% of the total taxable benefit value.

- Pay HMRC using your Accounts Office reference followed by 2613, ensuring cleared funds reach HMRC by 22 July 2026.

- Keep copies of all forms and your underlying calculations for at least six years.

- Begin planning for mandatory payrolling from April 2027, including briefing employees whose take-home pay will be affected.

Frequently Asked Questions

Do I need to file a P11D if all my employees’ benefits are payrolled?

You may not need individual P11D forms if all benefits were payrolled voluntarily, but you will almost certainly still need to file a P11D(b) to declare the Class 1A NIC due, including on the payrolled benefits. Do not assume that payrolling removes all year-end P11D obligations.

What is the Class 1A NIC rate for 2025/26?

The Class 1A NIC rate for the 2025/26 tax year is 15%, in line with the secondary employer NIC rate that increased from 13.8% in April 2025. Multiply the total taxable value of benefits across all P11D forms by 15% to arrive at the amount due.

Can I still file a P11D on paper?

No. HMRC no longer accepts paper P11D forms. All submissions must be made electronically, either through HMRC’s PAYE Online service or through compatible payroll software.

Will the P11D process really end in April 2027?

For most benefits, yes. Mandatory payrolling takes effect from 6 April 2027. However, two categories remain on P11D reporting beyond 2027: beneficial loans and living accommodation. Employers with these benefits will still have ongoing P11D obligations after the main transition.

Where can I get help with P11D filing and Class 1A NIC?

Protax Consultants are FCCA Chartered Certified accountants based in Wimbledon, London. Our payroll outsourcing service prepares and files P11D and P11D(b) returns, calculates your Class 1A liability, and manages your transition to mandatory payrolling for 2027. Fixed fee, no surprises. Call 020 8545 7451.

Muhammad Bilal is a Fellow Chartered Certified Accountant (FCCA) and Director of Protax Consultants, a London-based accounting firm specialising in tax advisory, compliance, and business accounting services.

Bilal qualified with the Association of Chartered Certified Accountants (ACCA) in 2009 and later achieved FCCA status after gaining extensive professional experience. With more than 13 years of experience in accounting, taxation, and auditing, he advises SMEs, landlords, contractors, and charities on tax planning, compliance, and financial management.

As a registered HMRC agent, Bilal assists clients with Self Assessment tax returns, corporation tax planning, VAT compliance, payroll services, and HMRC enquiries.

Bilal holds a BSc (Hons) in Applied Accounting and leads the audit and compliance function at Protax Consultants.

Company Verification:

Protax Consultants Ltd – Company Number 14701253

View Companies House Record